A property income tax return is the formal reporting of rental income and related expenses to HMRC through the Self Assessment system, and getting it right protects you from penalties while keeping your tax bill as low as legally possible. The official vehicle for this is the SA105 supplementary pages, which attach to your main Self Assessment return. Whether you rent out a single flat in Tonbridge or manage several buy-to-let properties, the rules are the same. Understanding the thresholds, allowable deductions, and filing process puts you firmly in control.

What are the income thresholds for reporting rental income to HMRC?

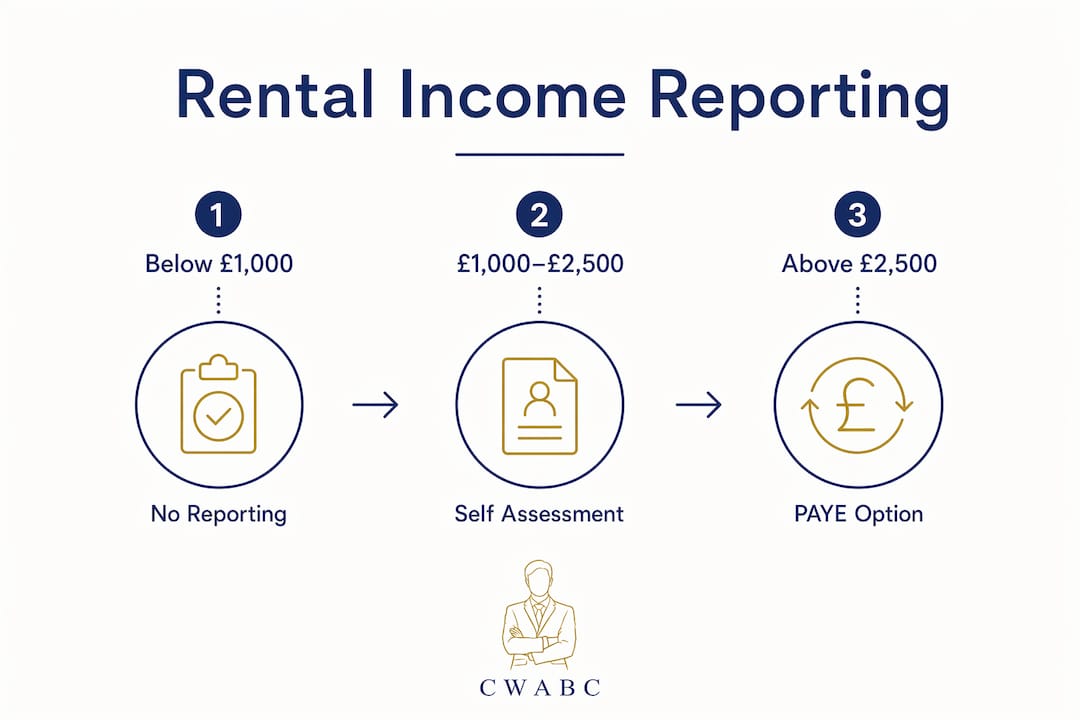

The threshold you fall into determines exactly how you report your rental income, and the rules are tiered based on your gross rental receipts before any expenses.

| Gross rental income | What you must do |

|---|---|

| Below £1,000 | No reporting required. The property allowance covers this fully. |

| £1,000 to £2,500 | Contact HMRC. A PAYE tax code adjustment may be possible. |

| Above £2,500 | Mandatory Self Assessment tax return required. |

Each band carries different obligations, so knowing where you sit is the first step.

Below £1,000: the property allowance

The £1,000 property allowance means rental income at this level is completely exempt from tax. You do not need to notify HMRC or file any return. This applies per individual, so a jointly owned property split between two owners each receiving under £1,000 would both qualify.

£1,000 to £2,500: the PAYE option

Landlords in this band can often avoid filing a full Self Assessment return. HMRC can instead collect the tax owed by adjusting your PAYE tax code, reducing your take-home pay slightly each month. You must contact HMRC proactively to arrange this. Many landlords miss this option entirely and file a full return when they do not need to.

Above £2,500: mandatory Self Assessment

Gross rental income above £2,500 triggers a mandatory Self Assessment tax return. This is where the SA105 form becomes your main tool. You must also notify HMRC by 5 october following the end of the relevant tax year, so for the 2025/26 tax year, the deadline to notify is 5 october 2026.

Pro Tip: If you are unsure which band applies to you, add up your total rental receipts before deducting any costs. That gross figure is what HMRC uses to determine your filing obligation.

Which expenses can landlords deduct on their property income tax return?

Allowable expenses are the costs you incur wholly and exclusively in renting out your property. Claiming them correctly is the single most effective way to reduce your taxable rental profit.

Allowable revenue expenses

Landlords can deduct a wide range of day-to-day running costs, including:

- Repairs and maintenance (fixing a broken boiler, repainting walls)

- Buildings and contents insurance premiums

- Letting agent fees and management charges

- Accountancy fees directly related to the rental business

- Ground rent and service charges

- Advertising costs to find tenants

- Utility bills you pay on behalf of tenants

Each of these reduces your taxable profit directly. Keep every receipt and invoice.

Capital improvements vs deductible expenses

This is where many landlords make costly errors. Capital improvements are not deductible against rental income. Replacing a worn-out kitchen with a like-for-like equivalent is a repair and is deductible. Upgrading to a premium fitted kitchen with added value is a capital improvement and is not. The distinction matters because incorrectly separating capital from revenue costs is one of the most common triggers for an HMRC enquiry. Capital expenditure may, however, reduce a capital gains tax liability when you eventually sell the property.

Property allowance vs actual expenses

You have a choice each year. You can claim the £1,000 property allowance as a flat deduction, or you can claim your actual allowable expenses. You cannot claim both. The right approach is to calculate both figures and choose whichever produces the lower taxable profit. If your actual expenses total £800, the £1,000 allowance wins. If they total £3,500, claiming actual expenses saves you more tax. For strategies on maximising deductions, the principle is always the same: calculate before you commit.

Pro Tip: Never default to the property allowance without checking your actual costs first. Landlords with insurance, agent fees, and repair bills almost always benefit more from claiming actual expenses.

How do you complete and file the SA105 property pages?

The SA105 supplementary pages are the official HMRC form for reporting UK property income. They attach to your main Self Assessment return and cover rental income, allowable expenses, and any other property-related receipts.

Step-by-step filing process

- Register for Self Assessment if you have not already done so. You can register online via GOV.UK. Do this by 5 october following the end of the tax year in which you first received rental income above the threshold.

- Gather your figures. Total up all rental receipts for the tax year (6 april to 5 april). Then list every allowable expense with supporting evidence.

- Complete the SA105 pages. Enter your total rental income, then your allowable expenses in the relevant boxes. The form separates expenses into categories such as repairs, insurance, and management fees.

- Choose your deduction method. Decide whether to claim the £1,000 property allowance or actual expenses. Enter the chosen figure in the correct box.

- Submit your return. File online via the HMRC Self Assessment portal by 31 january following the tax year end. Paper returns must reach HMRC by 31 october. Online filing is strongly recommended as it gives you an instant confirmation receipt.

- Pay any tax owed. The online system calculates your bill automatically. Payment is also due by 31 january.

Key filing deadlines

| Deadline | What it covers |

|---|---|

| 5 october | Notify HMRC you need to file (new registrations) |

| 31 october | Paper return submission deadline |

| 31 january | Online return submission and tax payment deadline |

Missing these dates triggers automatic penalties, starting at £100 for a late return.

Common mistakes to avoid on SA105

Getting the SA105 right matters more than most landlords realise. The most frequent errors include:

- Claiming capital improvements as revenue expenses

- Forgetting to include all rental income, including deposits retained at the end of a tenancy

- Mixing personal and property expenses

- Failing to declare income from short-term lets or holiday rentals

Each of these can trigger an HMRC enquiry. Attention to detail and accurate records are your best protection. If you need support with the Self Assessment filing process, working with a licensed accountant removes the guesswork entirely.

Pro Tip: File online rather than by post. The HMRC portal pre-populates some fields from previous returns, reduces errors, and gives you a submission reference number as proof of filing.

What records should landlords keep to support their tax return?

Good record keeping is not just about compliance. It makes preparing your return faster, reduces errors, and gives you a clear defence if HMRC ever asks questions.

Records to keep

Maintain the following for every property you let:

- Tenancy agreements for each letting period

- Rent receipts and bank statements showing all income received

- Invoices and receipts for every expense you claim

- Insurance documents and renewal certificates

- Mortgage statements if you claim finance costs

- Correspondence with letting agents including fee schedules

- Records of any work carried out, including contractor invoices and before/after photographs for repairs

Photographs of repair work are particularly useful. They demonstrate that a cost was genuinely a repair rather than an improvement, which is exactly the distinction HMRC looks for.

How long to keep records

Keeping records for at least five years after the 31 january filing deadline for the relevant tax year is the standard recommendation. For the 2025/26 tax year return filed in january 2027, you should retain records until at least january 2032. HMRC can open an enquiry within 12 months of filing, but that window extends significantly if errors or omissions are suspected.

Making Tax Digital and digital records

Making Tax Digital will affect some landlords from 2026 onwards. HMRC requires quarterly digital updates using approved software for property income taxpayers who meet the relevant income threshold. This makes digital record keeping not just good practice but a legal requirement for those in scope. Keeping digital records from the start, using software such as Xero, FreeAgent, or QuickBooks, puts you ahead of the requirement and makes your annual return far simpler to prepare. You can find detailed guidance on financial record keeping to set up a system that works for your property portfolio.

Pro Tip: Create a dedicated folder, physical or digital, for each property and each tax year. File every document as it arrives rather than hunting for receipts in january.

Key takeaways

Completing your property income tax return accurately depends on knowing your threshold, claiming the right expenses, and filing on time using the SA105 supplementary pages.

| Point | Details |

|---|---|

| Know your threshold | Gross rental income above £2,500 requires a full Self Assessment return via SA105. |

| Choose deductions carefully | Compare the £1,000 property allowance against actual expenses and claim whichever is lower. |

| File by 31 january | Online Self Assessment returns and tax payments are both due by 31 january each year. |

| Keep records for five years | Retain all rental agreements, receipts, and invoices for at least five years after filing. |

| Prepare for Making Tax Digital | Landlords above the income threshold must submit quarterly digital updates from 2026. |

My honest view on property income tax returns

I have worked with landlords at every level, from those renting out a single room to those managing a portfolio of buy-to-let properties. The pattern I see most often is not deliberate error. It is delay. Landlords leave everything until january, then scramble to find receipts from the previous april. The result is a return that misses deductions, mixes up capital and revenue costs, and creates unnecessary stress.

The capital versus revenue distinction is the area I find causes the most confusion. A landlord replaces a roof and assumes it is a repair. It may well be, if the roof was genuinely deteriorating and the replacement is like-for-like. But if they added insulation, extended the roof line, or upgraded the materials significantly, part of that cost becomes capital expenditure. Getting this wrong in either direction costs money. Overclaiming invites an HMRC enquiry. Underclaiming means paying more tax than you owe.

My practical advice is to treat your rental property like a small business from day one. Open a separate bank account for rental income and expenses. Reconcile it monthly. Take photographs of any repair work before and after. When you sit down to prepare your return, the figures are already there. The role of an accountant for landlords is not just to fill in a form. It is to review your records throughout the year, flag issues before they become problems, and make sure you claim everything you are entitled to.

One thing I would also encourage is proactive contact with HMRC if your rental income sits between £1,000 and £2,500. Most landlords in that band do not need to file a full return. A simple call or online message to HMRC can arrange a PAYE code adjustment instead. That saves time, reduces paperwork, and keeps your tax affairs simple. Do not assume you must file a full return just because you receive rental income.

— Chris

How Cwabc supports landlords with property income returns

Preparing and filing a property income tax return takes time, and the cost of getting it wrong is real. Cwabc works with landlords across Tonbridge and beyond, handling SA105 preparation, Self Assessment filing, and year-round bookkeeping so you stay compliant without the last-minute mess.

Whether you are filing for the first time or want to make sure you are claiming every allowable deduction, Cwabc’s landlord bookkeeping services give you a clear, organised system from the start. The team also supports landlords preparing for Making Tax Digital, so you are ready well before the 2026 deadlines. For a free, no-obligation conversation about your rental income tax, visit the Cwabc contact page and get in touch today.

FAQ

Who must file a property income tax return in the UK?

Landlords with gross rental income above £2,500 must file a Self Assessment tax return. Those earning between £1,000 and £2,500 may be able to use a PAYE tax code adjustment instead.

What is the SA105 form used for?

The SA105 supplementary pages are the HMRC form used to report UK property income within a Self Assessment return. They cover rental income, allowable expenses, and property-related allowances.

What is the deadline for filing a property income tax return?

Online Self Assessment returns must be submitted by 31 january following the end of the tax year. Paper returns are due by 31 october. New landlords must notify HMRC by 5 october.

Can I deduct mortgage payments from my rental income?

Mortgage capital repayments are not deductible. Landlords can claim a tax credit based on mortgage interest, but the rules changed significantly from 2020 onwards. The credit is now restricted to the basic rate of income tax.

Do I need to keep records if I use the property allowance?

Yes. Even if you claim the £1,000 property allowance rather than actual expenses, you should retain records of your rental income for at least five years. HMRC can request evidence of your figures at any point during that period.

Need help?

Filing a property income tax return does not need to be stressful. Cwabc offers a free, no-obligation conversation to help you understand your obligations and get your records in order. Get in touch today and let us take the complexity off your plate.