An annual tax return for landlords is the formal process of declaring rental income and allowable expenses to HM Revenue and Customs (HMRC) each year to calculate and pay the correct amount of income tax. In the UK, this is done through Self Assessment, a system where you report your own income rather than having tax deducted automatically. Most landlords earning rental income above £1,000 per year must complete this return. Understanding what is annual tax return landlord means in practice, and what you need to report, is the first step to staying compliant and avoiding penalties.

What is an annual tax return for landlords?

An annual tax return for landlords is a Self Assessment return submitted to HMRC that declares all rental income received and any allowable expenses claimed during the tax year. The tax year in the UK runs from 6 april to 5 april the following year. Most UK landlords must register with HMRC and complete this return each year to pay income tax on their rental profits.

The return covers more than just rent collected. You also declare any other income sources, such as employment or self-employment earnings, alongside your property income. HMRC uses the combined figure to calculate your total tax liability for the year. Getting this right from the start avoids costly corrections later.

Two key deadlines apply. Paper returns must be submitted by 31 october following the end of the tax year. Online submissions are due by 31 january, which is the deadline most landlords use. Any tax owed is also due by 31 january, so missing this date means both a late filing penalty and interest on unpaid tax.

What rental income must landlords declare?

Taxable rental income is any money you receive from letting a property, including rent, tenant fees, and any services you charge for. The UK property allowance lets landlords earn up to £1,000 tax-free before they need to declare it. Above that threshold, all rental income must be reported and taxed at your marginal income tax rate.

Rental income is added to your other income sources before tax is calculated. This means a landlord who also works full-time could find their rental profit pushes them into a higher tax band. The tax rates that apply are the standard income tax bands: 20% for basic rate, 40% for higher rate, and 45% for additional rate taxpayers.

Many landlords overlook income sources beyond basic rent. The following are all taxable and must be declared:

- Payments for services such as cleaning or gardening included in the tenancy agreement

- Charges for utilities or broadband where the landlord pays the bill and recovers the cost from tenants

- Premiums received for granting a lease

- Income from furnished holiday lettings, which has its own specific tax rules

- Payments received when a tenant breaks a lease early

Missing any of these is a common trigger for HMRC queries. Keeping a clear record of every payment received, not just the monthly rent, protects you if HMRC asks questions.

What expenses can landlords deduct to reduce their tax bill?

Allowable expenses are costs you can deduct from your rental income before calculating the tax you owe. Expenses must be incurred wholly and exclusively for the purpose of letting the property. Personal costs, even if partly related to the property, cannot be claimed.

The distinction between repairs and improvements is one of the most misunderstood areas of landlord tax. A repair restores something to its original condition and is fully deductible. An improvement upgrades the property beyond its original state and is treated as capital expenditure, meaning it cannot be deducted from rental income. UK landlords must distinguish repairs from improvements accurately, as this also affects future capital gains calculations when you sell.

Common allowable expenses include:

- Mortgage interest (subject to the restriction rules introduced since 2017, now replaced by a 20% tax credit)

- Letting agent fees and property management costs

- Buildings and contents insurance premiums

- Repairs and maintenance, such as fixing a boiler or repainting walls

- Accountancy fees for preparing your tax return

- Ground rent and service charges on leasehold properties

- Utility bills paid by the landlord

For landlords with mixed-use properties, understanding how to split costs correctly matters. Guidance on managing mixed-use expenses can help you avoid overclaiming or underclaiming on shared costs.

Pro Tip: Keep a dedicated folder, physical or digital, for every expense receipt related to your rental property. HMRC can request evidence going back several years, and a missing receipt for a legitimate cost means you cannot claim it.

Deductions directly reduce your taxable profit. A landlord with £12,000 rental income and £4,000 in allowable expenses pays tax on £8,000, not £12,000. Getting your expenses right is one of the most practical ways to reduce your annual tax bill legally.

How does the landlord tax filing process work?

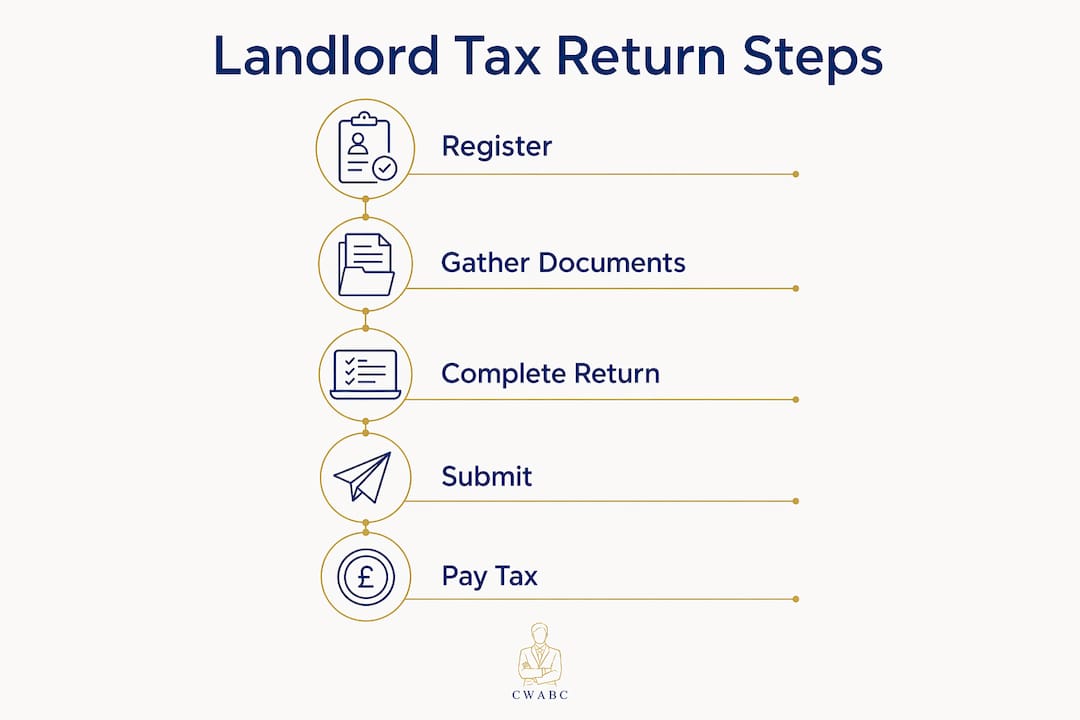

The landlord tax filing process begins with registering for Self Assessment with HMRC if you have not already done so. You must register by 5 october in the second tax year after you started receiving rental income. Failing to register on time can result in a penalty.

Once registered, you file your return either online through HMRC’s Government Gateway or by paper. The online route is faster, more flexible, and gives you until 31 january rather than 31 october for paper. The steps are straightforward:

- Log in to your HMRC Government Gateway account (or create one if new).

- Complete the SA100 main tax return form.

- Add the SA105 supplementary pages for UK property income.

- Enter your total rental income and all allowable expenses.

- Review the calculated tax figure and submit before the deadline.

- Pay any tax owed by 31 january.

From april 2026, the annual tax obligations for landlords will change significantly. Making Tax Digital for Income Tax Self Assessment (MTD ITSA) will require quarterly reporting for landlords with income above £50,000. This means submitting income and expense updates to HMRC every three months using compatible software, followed by a final annual declaration. The annual declaration replaces the traditional single Self Assessment return for those within scope.

Pro Tip: Do not wait until january to start your return. Gather your rental income records and expense receipts in april or may, right after the tax year ends. Filing early means any unexpected tax bills give you months to plan payment rather than days.

Missing the 31 january deadline triggers an automatic £100 penalty, even if no tax is owed. Further penalties apply at three months, six months, and twelve months late. Interest accrues daily on unpaid tax. The 2026 tax guide for landlords covers how MTD ITSA changes these obligations in detail.

Common mistakes landlords make on tax returns

Errors on landlord tax returns fall into predictable patterns. Many landlords fail to claim all allowable expenses or miss recording some rental income, which leads to either overpayment or penalties. Both outcomes are avoidable with good habits.

The most frequent mistakes include:

- Missing income: Forgetting to declare one-off payments, such as a lease premium or a tenant’s contribution to repairs

- Overclaiming improvements: Treating a kitchen renovation as a repair rather than capital expenditure

- Underclaiming expenses: Not claiming accountancy fees, ground rent, or travel costs for property inspections

- Poor records: Losing receipts or failing to separate personal and rental finances

- Joint ownership errors: Where a property is jointly owned, each owner must declare their share of income and expenses separately on their own return

Detailed, organised records form the basis of a stress-free tax return and reduce the risk of HMRC penalties. This is not just good advice. It is the single most practical thing you can do to protect yourself.

Accounting software such as Xero, FreeAgent, or QuickBooks makes record keeping significantly easier. These tools let you categorise income and expenses throughout the year, so your return is largely complete before you even log into HMRC. For landlords preparing for MTD ITSA, using compatible software now means the transition in 2026 is far less disruptive. Cwabc offers accounting software setup support in Kent for landlords who want to get this right from the start.

Pro Tip: Open a separate bank account solely for rental income and expenses. This one step eliminates the most common source of bookkeeping chaos: mixing personal and property finances.

UK vs US landlord tax returns: what are the key differences?

The UK and US tax systems both require landlords to declare rental income annually, but the rules differ in important ways. US landlords report rental income on Schedule E (Form 1040) and claim depreciation over 27.5 years as a mandatory deduction. UK landlords do not have an equivalent mandatory depreciation deduction for residential property.

Depreciation is a mandatory deduction for US residential rental property under IRS rules, recaptured at sale at a maximum 25% rate. Failing to account for this correctly creates significant tax liabilities when a US property is sold. UK landlords face capital gains tax on property sales instead, with different rates and reliefs applying.

Passive activity loss rules in the US limit how much rental loss most individuals can offset against other income. US rental losses are limited under passive activity loss rules unless the landlord qualifies as a real estate professional or actively participates. The UK has no direct equivalent restriction of this kind for individual landlords.

| Feature | UK landlord | US landlord |

|---|---|---|

| Filing form | SA100 + SA105 | Schedule E (Form 1040) |

| Depreciation | Not applicable for residential property | Mandatory over 27.5 years |

| Self-employment tax | Not applicable on rental income | Not applicable on Schedule E income |

| Loss offset rules | No passive activity restriction | Passive activity loss rules apply |

| Quarterly reporting | Required from april 2026 (MTD ITSA) | Not required |

| Tax-free allowance | £1,000 property allowance | No direct equivalent |

For landlords managing properties in both countries, the differences in depreciation treatment alone make specialist advice worth seeking. The business tax guide for small business owners in 2026 covers cross-border tax considerations in more depth.

Key takeaways

Filing an annual tax return as a landlord requires declaring all rental income, claiming only allowable expenses, and submitting to HMRC by 31 january each year, with quarterly digital reporting required from april 2026.

| Point | Details |

|---|---|

| Register for Self Assessment | Register with HMRC by 5 october in your second year of receiving rental income. |

| Declare all rental income | Report rent, fees, and any other payments received, not just monthly rent. |

| Claim allowable expenses | Deduct costs incurred wholly and exclusively for letting, including repairs and agent fees. |

| Know your deadlines | Online returns are due 31 january; paper returns by 31 october each year. |

| Prepare for MTD ITSA | From april 2026, landlords earning above £50,000 must submit quarterly digital updates. |

Why I think most landlords leave money on the table every year

After working with landlords across Kent and beyond, the pattern I see most often is not fraud or deliberate error. It is simply underconfidence. Landlords either claim too little because they are not sure what is allowed, or they rush the return in january and miss things entirely.

The mortgage interest restriction is a good example. Many landlords still do not fully understand that the old system of deducting mortgage interest directly from rental income was phased out. The current system gives a 20% tax credit instead, which affects higher and additional rate taxpayers significantly. Getting this wrong, in either direction, changes your tax bill materially.

The MTD ITSA change coming in april 2026 is not something to fear. It is actually an opportunity. Quarterly reporting forces you to keep records in real time rather than scrambling at year end. Landlords who prepare accounts properly throughout the year will find the annual declaration almost effortless. Those who leave everything to january will find the quarterly system genuinely stressful.

My honest view is that most landlords benefit from professional support, not because the return is impossibly complex, but because the cost of getting it wrong, whether through missed deductions or HMRC penalties, almost always exceeds the cost of good advice. Understanding the role of an accountant for landlords is a practical starting point if you are unsure whether professional help is right for you.

— Chris

How Cwabc helps landlords file with confidence

Cwabc is a licensed bookkeeper and accountant based in Tonbridge, specialising in Self Assessment returns and bookkeeping for landlords. Whether you are filing your first return or preparing for the MTD ITSA transition in 2026, Cwabc offers clear, jargon-free support tailored to your situation.

From organising your rental records to submitting your return accurately and on time, Cwabc takes the stress out of the process. Explore the bookkeeping FAQs for landlords to get answers to the most common questions, or visit the Self Assessment tax return service to find out how Cwabc can support your annual filing. Upfront pricing, local expertise, and no surprises.

FAQ

What is a Self Assessment tax return for landlords?

A Self Assessment tax return is the annual form landlords submit to HMRC to declare rental income and expenses and calculate income tax owed. Most landlords earning above £1,000 in rental income must complete one each year.

When is the deadline for a landlord’s tax return?

The online Self Assessment deadline is 31 january following the end of the tax year. Paper returns must be submitted by 31 october. Any tax owed is also due by 31 january.

What expenses can a landlord claim on their tax return?

Landlords can claim expenses incurred wholly and exclusively for letting the property, including mortgage interest (as a 20% tax credit), repairs, insurance, letting agent fees, and accountancy costs. Improvements to the property are not deductible as expenses.

What is Making Tax Digital and how does it affect landlords?

Making Tax Digital for Income Tax Self Assessment (MTD ITSA) requires landlords with income above £50,000 to submit quarterly digital income and expense updates to HMRC from april 2026. An annual declaration then finalises the tax position for the year.

Do landlords need an accountant to file their tax return?

Landlords are not legally required to use an accountant, but professional support reduces the risk of errors, missed deductions, and penalties. An accountant familiar with property income can also identify legitimate savings that many landlords overlook.