A small business tax deadline calendar is a structured record of every tax filing and payment date your business must meet throughout the year. Without one, it is easy to lose track of Self Assessment submissions, VAT returns, Corporation Tax payments, and PAYE obligations. Missing these dates costs money. HMRC applies escalating penalties and interest charges for late filings and payments, and those costs add up quickly. The UK tax year runs from 6 april to 5 april the following year, which means your deadlines do not follow a simple calendar year. A well-organised tax schedule gives you clarity, reduces stress, and keeps you compliant.

What are the main small business tax deadlines in the UK?

Tax obligations vary depending on whether you are a sole trader, a limited company, or a VAT-registered business. Each structure carries its own set of deadlines, and your accounting period affects the exact dates. Getting clear on which rules apply to you is the first step to building a reliable small business tax schedule.

Self Assessment deadlines

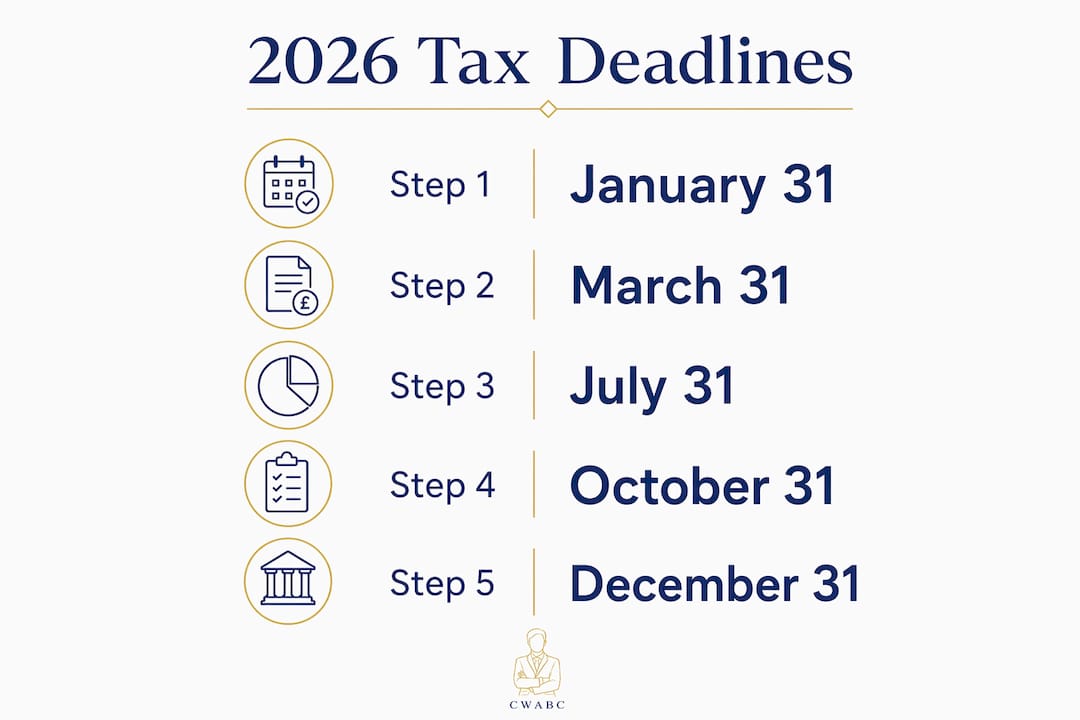

Self Assessment applies to sole traders, partners, and directors with income outside PAYE. For the 2025/26 tax year, the key dates are:

- 5 october 2026: deadline to register for Self Assessment if you are newly self-employed

- 31 october 2026: deadline for paper tax return submission

- 31 january 2027: deadline for online filing and full payment of tax owed

- 31 july 2027: second payment on account, where applicable

Payments on account are advance payments toward your next tax bill, due on 31 january and 31 july each year. Many sole traders are caught off guard by these. If your previous year’s tax bill exceeded £1,000, you will likely owe payments on account on top of your balancing payment.

VAT return deadlines

VAT returns and payments are due one calendar month plus seven days after the end of each VAT accounting period. For a business on quarterly VAT returns with periods ending in march, june, september, and december, the submission and payment deadlines fall in may, august, november, and january respectively. Missing a VAT deadline triggers a surcharge or penalty points under HMRC’s current system, so these dates belong in your calendar from day one.

Corporation Tax and Companies House filings

Limited companies face a different set of deadlines. Corporation Tax is due nine months and one day after the end of the accounting period. The CT600 return must be filed within twelve months of the accounting period end. Companies House also requires annual accounts and a confirmation statement, with separate deadlines tied to your company’s incorporation date. Missing Companies House filings can result in your company being struck off the register.

PAYE and National Insurance

Employers must pay PAYE and National Insurance Contributions to HMRC by the 19th of each month if paying by post, or the 22nd if paying electronically. Real Time Information (RTI) submissions must be made on or before each pay day. These are recurring monthly obligations that belong in every employer’s tax calendar.

| Tax obligation | Who it applies to | Key deadline |

|---|---|---|

| Self Assessment online filing | Sole traders, directors | 31 january following tax year end |

| Self Assessment payment on account | Sole traders with bill over £1,000 | 31 january and 31 july |

| VAT return and payment | VAT-registered businesses | One month and seven days after period end |

| Corporation Tax payment | Limited companies | Nine months and one day after accounting period |

| CT600 filing | Limited companies | Twelve months after accounting period |

| PAYE and NIC payment | Employers | 22nd of each month (electronic) |

| Companies House accounts | Limited companies | Nine months after accounting period |

How to build a personalised tax deadline calendar

A personalised tax deadline calendar works because it reflects your specific accounting period, VAT quarter, and payroll cycle rather than a generic list of dates. Generic checklists are a starting point. Your own calendar is what actually keeps you compliant.

-

Identify your accounting period. Your year-end date drives most of your deadlines. Write it down and work backwards from it to calculate your Corporation Tax payment date, CT600 filing date, and Companies House submission date.

-

Confirm your VAT quarters. Log into your HMRC VAT online account to confirm which months your VAT periods end. Add the submission and payment deadlines for each quarter to your calendar immediately.

-

Add Self Assessment dates. If you complete a Self Assessment return, add 5 october (registration), 31 october (paper), and 31 january (online and payment) for the relevant tax year. If you pay on account, add 31 july as well.

-

Include PAYE and payroll dates. For each pay run, note the RTI submission date and the PAYE payment deadline. These repeat monthly, so set them as recurring entries.

-

Link each deadline to a preparation task. A deadline entry on its own is not enough. Add a reminder two to four weeks before each date prompting you to gather receipts, reconcile accounts, or check your bookkeeping software is up to date.

-

Use digital tools to automate reminders. Google Calendar, Microsoft Outlook, and HMRC’s own online account all support reminder notifications. Set alerts at four weeks, two weeks, and one week before each deadline.

Pro Tip: Set your calendar reminders to trigger earlier than you think you need. If a deadline is 31 january, set your first reminder for 2 january. That gives you the full month to resolve any issues without panic.

HMRC also sends reminders by post and through your online account, but do not rely on these alone. Postal reminders can be delayed, and online notifications are easy to miss. Your own calendar is your primary system.

Why consistent bookkeeping supports your tax deadline management

Live bookkeeping throughout the year is the foundation of effective tax deadline management. When your records are current, you know your tax position at any point in the year. You are not scrambling to reconstruct months of transactions in january.

Panicked last-minute filing often leads to missed expense claims and attracts increased HMRC scrutiny during audits. Consistent bookkeeping avoids both problems. When your income and expenses are recorded weekly or monthly, your figures are accurate and your allowable deductions are captured in full.

Bookkeeping also supports your obligations under Making Tax Digital (MTD). HMRC’s MTD programme requires businesses above the VAT threshold to keep digital records and submit returns using compatible software. From april 2026, MTD for Income Tax Self Assessment (MTD for ITSA) begins its phased rollout for sole traders and landlords with income above £50,000. Keeping live digital records now puts you ahead of that requirement.

“The businesses that find tax deadlines stressful are almost always the ones that leave their bookkeeping until the last few weeks of the tax year. The ones that stay calm are the ones with records that are already up to date.”

Here is what consistent bookkeeping prevents:

- Missed expense claims. Receipts get lost. Transactions get forgotten. Regular reconciliation captures everything while it is fresh.

- Incorrect VAT figures. Errors in VAT returns can trigger penalties and interest. Monthly reconciliation catches mistakes before submission.

- Surprise tax bills. When you know your profit in real time, your tax liability is never a shock. You can set money aside throughout the year.

- HMRC enquiries. Clean, consistent records reduce the risk of HMRC opening an investigation into your affairs.

Pro Tip: Reconcile your bank account at least once a month. It takes less than an hour when records are current, and it means your tax return figures are already accurate by the time the deadline arrives.

The link between bookkeeping and tax deadlines is direct. Every entry you make in your bookkeeping software is one less thing to do under pressure in january.

Common mistakes that cause small businesses to miss tax deadlines

Missing a tax deadline is rarely deliberate. It usually comes down to one of a small number of predictable errors. Knowing what they are makes them easy to avoid.

-

Relying on memory. Tax deadlines do not move to suit your schedule. Relying on memory rather than a written or digital calendar is the single most common cause of missed filings. Write every date down.

-

Confusing filing deadlines with payment deadlines. These are not always the same date. For Self Assessment, the online filing deadline and the payment deadline both fall on 31 january, but Corporation Tax payment is due before the CT600 filing deadline. Treat them as separate entries in your calendar.

-

Ignoring changes in your business circumstances. If you register for VAT, take on employees, or change your accounting year-end, your deadlines change. Review your tax calendar whenever your business structure or circumstances change.

-

Failing to register on time. You must register for Self Assessment by 5 october in the tax year after you became self-employed. Missing this date triggers an automatic penalty, even if you owe no tax.

-

Not registering for Making Tax Digital. MTD for VAT is already mandatory for VAT-registered businesses. MTD for ITSA is coming for sole traders and landlords. Failing to register on time will result in penalties. Check your obligations now rather than waiting for a reminder that may not arrive.

-

Leaving preparation too late. A deadline in your calendar only helps if you start preparing in advance. Build preparation tasks into your calendar alongside the deadline itself.

The fix for all of these is the same: a maintained calendar, updated records, and a habit of reviewing both regularly. If you are unsure whether you are meeting all your obligations, a tax professional can review your position quickly.

What to do if you miss a small business tax deadline

Missing a deadline is not ideal, but acting quickly limits the damage. HMRC applies escalating penalties for late filings and payments, with interest accruing on overdue amounts. The longer you wait, the more it costs.

-

File or pay as soon as possible. Even if you cannot pay the full amount owed, filing the return immediately stops the late filing penalty from increasing. A late payment penalty is separate from a late filing penalty.

-

Contact HMRC directly. If you have a genuine reason for missing a deadline, such as a serious illness or a bereavement, HMRC may accept a reasonable excuse and cancel the penalty. Contact them as soon as you can and explain your circumstances.

-

Consider a Time to Pay arrangement. If you cannot pay your tax bill in full, HMRC offers Time to Pay arrangements that allow you to spread payments over an agreed period. You must contact HMRC before the debt is passed to a debt collection agency.

-

Seek professional support. A licensed bookkeeper or accountant can communicate with HMRC on your behalf, help you understand the penalty structure, and negotiate where possible. This is particularly useful if you have multiple missed deadlines or a complex tax position.

-

Review and update your calendar. Once the immediate issue is resolved, go back to your tax calendar and identify what went wrong. Add earlier reminders, update your preparation tasks, and consider whether your bookkeeping process needs to change.

The most important thing is not to ignore the situation. HMRC does not forget, and penalties do not disappear on their own.

Key takeaways

A maintained small business tax deadline calendar, combined with live bookkeeping, is the most reliable way to avoid HMRC penalties and stay compliant throughout the year.

| Point | Details |

|---|---|

| Know your deadlines by business type | Sole traders, limited companies, and VAT-registered businesses each face different filing and payment dates. |

| Self Assessment has multiple key dates | Register by 5 october, file online by 31 january, and pay on account by 31 july where applicable. |

| VAT returns follow a fixed pattern | Submissions and payments are due one month and seven days after each VAT period ends. |

| Live bookkeeping prevents last-minute errors | Consistent records mean accurate figures, captured expenses, and no surprise tax bills. |

| Act immediately if you miss a deadline | File or pay as soon as possible, contact HMRC, and consider a Time to Pay arrangement if needed. |

Why I think most small businesses make this harder than it needs to be

Working with sole traders and small business owners in and around Tonbridge, I see the same pattern repeatedly. The tax deadline arrives, the panic sets in, and the next few weeks are spent reconstructing months of transactions from bank statements and shoeboxes of receipts. It is exhausting, and it is entirely avoidable.

The businesses that handle tax deadlines calmly are not the ones with more time or more money. They are the ones with a simple system. A calendar with the right dates. Bookkeeping that is done weekly rather than annually. A habit of checking both regularly.

What surprises most people is how little time good bookkeeping actually takes when it is done consistently. Fifteen minutes a week is enough for most sole traders. That fifteen minutes in week one saves three stressful days in january.

I also think there is a wider mindset issue at play. Many small business owners see tax as something that happens to them rather than something they manage. Shifting that perspective changes everything. When you treat your tax calendar as a live tool rather than a list of threats, you stop dreading deadlines and start planning around them.

The preparation process for a tax return does not have to be complicated. But it does have to start before the deadline is two weeks away. If you take one thing from this article, let it be this: build your calendar now, link it to your bookkeeping, and review it every month. That habit alone will save you more stress and money than any other single change you could make.

— Chris

Need help staying on top of your tax deadlines?

Managing a tax deadline calendar alongside running a business is a lot to keep on top of. Cwabc works with sole traders and small business owners across Kent and beyond, providing clear, jargon-free bookkeeping and accounting support that keeps you compliant and organised throughout the year.

From setting up your bookkeeping in Tonbridge to handling VAT returns, Self Assessment, payroll, and Making Tax Digital compliance, Cwabc offers upfront pricing and personalised support with no surprises. If you are not sure where to start, or if you have missed a deadline and need help getting back on track, get in touch for a free, no-obligation conversation. Contact Cwabc today and take the first step toward stress-free tax management.

FAQ

What is a small business tax deadline calendar?

A small business tax deadline calendar is a structured record of all the tax filing and payment dates your business must meet with HMRC and Companies House throughout the year. It covers Self Assessment, VAT, Corporation Tax, PAYE, and any other obligations relevant to your business type.

When is the Self Assessment deadline for 2026?

For the 2025/26 tax year, the online Self Assessment filing and payment deadline is 31 january 2027. The paper return deadline is 31 october 2026, and new registrations must be submitted by 5 october 2026.

How often do VAT returns need to be submitted?

Most VAT-registered businesses submit quarterly VAT returns, with each return and payment due one calendar month and seven days after the end of the VAT period. Some businesses file monthly or annually depending on their VAT scheme.

What happens if I miss a tax deadline?

HMRC applies escalating penalties for late filings and interest on overdue payments. Filing or paying as soon as possible after a missed deadline limits the financial impact. Contact HMRC promptly if you have a genuine reason for the delay, as they may accept a reasonable excuse.

Do I need different deadlines for a limited company versus a sole trader?

Yes. Deadlines differ significantly between sole traders and limited companies. Sole traders follow Self Assessment deadlines, while limited companies must manage Corporation Tax payment, CT600 filing, and Companies House submissions, all tied to their specific accounting period end date.