Making Tax Digital for Income Tax Self Assessment (MTD for ITSA) is the HMRC programme that requires UK landlords to keep digital records and submit quarterly income and expense updates, replacing the traditional annual Self Assessment return. From 6 april 2026, this is mandatory for unincorporated landlords with gross qualifying income above £50,000 per year. The change affects how you record rental income, how often you report to HMRC, and which software you use. If you rent out property and your income is approaching that threshold, the time to prepare is now, not next January.

Who needs to comply with making tax digital for landlords?

MTD for ITSA applies to unincorporated landlords whose gross qualifying income exceeds the current threshold. Gross qualifying income includes rental income from UK property, plus any self-employment income you earn. HMRC uses your previous tax year’s figures to determine whether you must comply in the current year.

The thresholds reduce over time, bringing more landlords into scope each year. The table below shows the phased rollout:

| Tax year | Income threshold | Who is affected |

|---|---|---|

| 2026/27 | Over £50,000 | Landlords and self-employed above this combined threshold |

| 2027/28 | Over £30,000 | Wider group of landlords brought into scope |

| 2028/29 | Over £20,000 | Near-universal coverage for unincorporated landlords |

The phased approach gives landlords with lower incomes more time to prepare. That said, waiting until the year your threshold is reached is not a good plan. Getting your records in order early means far less stress when the deadline arrives.

Limited company landlords sit outside the MTD for Income Tax rules entirely. They continue to submit corporation tax returns separately, as limited company landlords remain outside the MTD for Income Tax scope. MTD for Corporation Tax is a separate government project with its own timeline. If you own property through a limited company, your obligations under this particular scheme do not apply yet.

What are the digital record keeping and quarterly reporting requirements?

The core change under MTD for ITSA is straightforward: you replace your single annual tax return with four quarterly updates and one final year-end declaration. Each quarterly update covers the income and expenses for that period, submitted through HMRC-approved MTD-compatible software.

The quarterly deadlines follow a fixed pattern after your accounting period starts. The first quarterly deadline was 7 august 2026 for landlords who entered the scheme from 6 april 2026. Subsequent deadlines fall every three months after that. Missing a deadline triggers a penalty point, so knowing your dates in advance is non-negotiable.

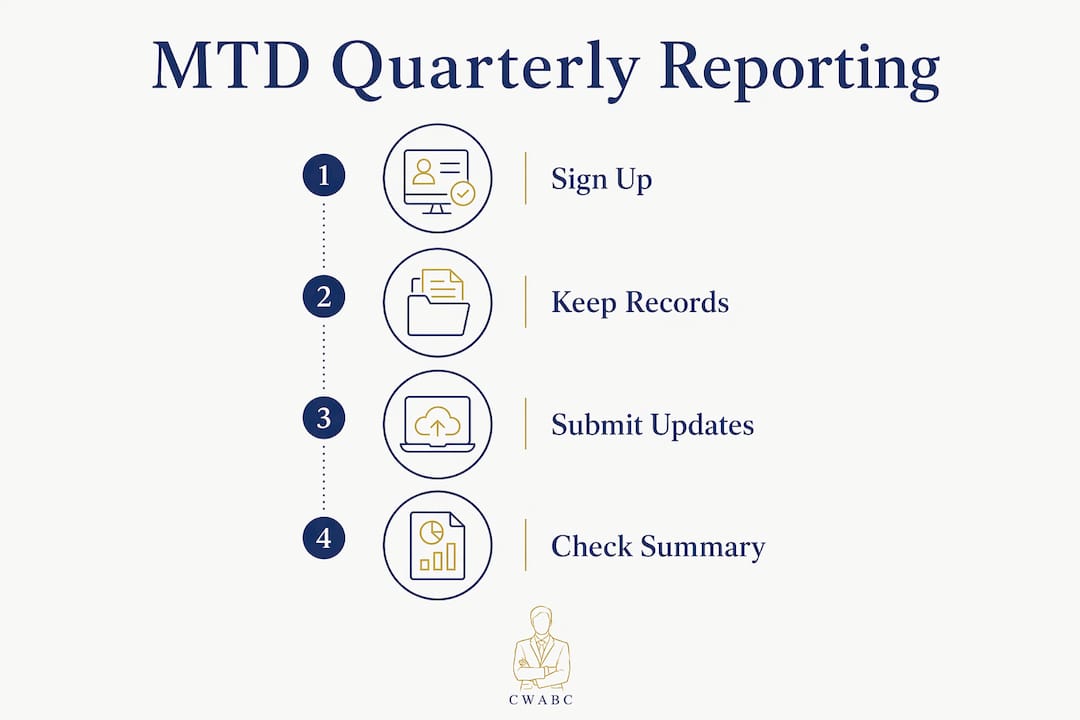

Here is the step-by-step reporting process you follow each year:

- Record income and expenses digitally throughout the quarter using your chosen MTD-compatible software.

- Submit your quarterly update to HMRC through the software before the relevant deadline.

- Review the estimated tax bill that the MTD system generates after each update. This figure helps you plan your cash flow, but it is not your final liability.

- Repeat for all four quarters of your accounting year.

- Submit the final declaration after the tax year ends. This is where your actual tax liability is calculated, allowances are applied, and any adjustments are made.

- Pay any tax owed by 31 january following the end of the tax year, as with the current Self Assessment system.

Quarterly updates are interim reports, not final tax filings. The tax liability is calculated only at the final declaration stage, and landlords should review quarterly data carefully to avoid errors that compound over the year.

Pro Tip: Treat each quarterly update like a progress check on your finances. Catching a miscategorised expense in quarter two is far easier than untangling twelve months of records in january.

What exemptions and special circumstances apply to landlords?

Not every landlord must comply with MTD for ITSA. HMRC recognises that digital filing is not always practical for everyone, and exemptions exist for qualifying circumstances.

You may be eligible for a digital exclusion exemption if:

- Age or disability makes it unreasonably difficult to use digital tools.

- Location means you have no reliable internet access.

- Religious beliefs prevent you from using computers or electronic systems.

- Other personal circumstances that HMRC considers on a case-by-case basis.

HMRC evaluates exemptions individually, so there is no automatic approval. You must apply and provide evidence of your circumstances. If granted an exemption, you continue filing paper Self Assessment returns as before.

Limited companies are categorically exempt from MTD for Income Tax. They pay Corporation Tax, not Income Tax, so the MTD for ITSA rules simply do not apply to them.

Voluntary compliance is also an option. Landlords below the current threshold can choose to join MTD early. Doing so gives you time to learn the system without the pressure of a mandatory deadline. Early adopters tend to find the transition much smoother than those who wait until the last moment.

Pro Tip: If you think you might qualify for an exemption, apply to HMRC well before your compliance date. Processing takes time, and you do not want to miss a quarterly deadline while waiting for a decision.

Failing to comply without an exemption carries real consequences. Each missed submission earns a penalty point, and four points trigger a £200 fine. Points accumulate across missed quarterly updates and final declarations, so consistent non-compliance becomes expensive quickly.

How to select MTD-compatible software for landlord tax compliance

HMRC does not provide free MTD software. Every landlord in scope must choose from commercially available, HMRC-approved products. Spreadsheets alone are non-compliant unless linked to HMRC’s systems through bridging software.

The main categories of software available to landlords are:

- Dedicated landlord accounting software: Built specifically for property income tracking. These products handle rental income, allowable expenses, and multiple properties within one system.

- General bookkeeping platforms: Products such as Xero, FreeAgent, and QuickBooks offer MTD-compatible modules suitable for landlords who also run a self-employed business alongside their property income.

- Bridging software: A middle-ground option that connects an existing spreadsheet to HMRC’s MTD API. Useful if you are comfortable with spreadsheets and do not want to rebuild your records from scratch.

When choosing software, consider these factors:

- Portfolio size: A landlord with two properties has different needs from one managing fifteen.

- Complexity: Do you have mixed income sources, furnished holiday lets, or overseas properties? Some platforms handle these better than others.

- Cost: Prices vary considerably. Entry-level apps suit simple portfolios; more capable platforms cost more but save time on complex returns.

- Ease of use: Software you will actually use consistently is better than a feature-rich platform you find confusing.

Beginning to use MTD-compliant software ahead of your mandatory start date is the single most effective step you can take. Delaying software adoption increases the chance of errors and penalties when deadlines arrive.

What practical steps should landlords take to prepare for MTD?

Preparation is the difference between a calm compliance process and a last-minute scramble. The steps below give you a clear path from where you are now to full compliance.

- Check your income against the threshold. Add your gross rental income and any self-employment income from the previous tax year. If the total exceeds £50,000, you are in scope now.

- Register for MTD using your Self Assessment credentials. You will need your National Insurance number, the start date of your property income, and your preferred accounting method (cash or accruals).

- Choose and set up your MTD-compatible software. Select a product that suits your portfolio and connect it to your HMRC account through the software’s MTD sign-up process.

- Begin recording all income and expenses digitally from day one. Do not keep paper records alongside digital ones. A single, consistent system prevents confusion and errors.

- Submit each quarterly update on time. Diarise your deadlines. The first falls on 7 august 2026 for those who entered the scheme in april 2026, with subsequent deadlines every three months.

- Review your figures before each submission. The MTD system generates an estimated tax bill after each update. Use it to set aside funds and spot anything that looks wrong.

- File your final declaration by 31 january. This replaces your old Self Assessment return and confirms your actual tax liability for the year.

- Work with an accountant who understands landlord MTD compliance. The role of an accountant for landlords goes beyond filing. A good adviser helps you categorise expenses correctly, choose the right software, and avoid the penalty points that come from missed or inaccurate submissions.

From april 2026, landlords must sign up using existing Self Assessment credentials and begin digital record keeping immediately. The registration process is straightforward, but it must happen before your first quarterly deadline, not after.

Key takeaways

Making Tax Digital for Income Tax Self Assessment requires UK landlords with gross qualifying income above £50,000 to keep digital records, submit four quarterly updates, and file a final annual declaration through HMRC-approved software from april 2026.

| Point | Details |

|---|---|

| Income thresholds reduce over time | The £50,000 threshold drops to £30,000 in 2027 and £20,000 in 2028, bringing more landlords into scope each year. |

| Quarterly updates are not final tax bills | HMRC calculates your actual liability only at the final declaration stage; quarterly updates are progress reports. |

| HMRC provides no free software | Landlords must choose from approved commercial products; spreadsheets alone are non-compliant without bridging software. |

| Exemptions exist but require application | Digital exclusion on grounds of age, disability, location, or religious belief must be applied for and evidenced. |

| Penalty points accumulate quickly | Each missed submission earns one point, and four points trigger a £200 fine. |

Why MTD is a bigger opportunity than most landlords realise

I have spoken with a lot of landlords over the years, and the reaction to Making Tax Digital tends to follow a predictable pattern. First comes the frustration: “Why do I have to report four times a year instead of once?” Then comes the worry: “What if I get it wrong?” Both reactions are understandable. Neither is particularly useful.

Here is what I have actually seen happen when landlords get set up properly and early. They start to see their rental finances clearly, often for the first time. When you record income and expenses every quarter rather than scrambling through twelve months of bank statements in january, patterns emerge. You notice which property costs are rising. You spot expenses you forgot to claim. You have a running estimate of your tax bill, so nothing comes as a shock.

The landlords who struggle with MTD are almost always the ones who delay. They wait until the deadline is close, rush to pick software, and then try to reconstruct months of records in a hurry. That is where errors creep in and where penalty points start to accumulate.

My honest advice is this: treat MTD as a prompt to get your finances properly organised, not as a burden imposed on you. The quarterly rhythm, once established, takes far less time than the annual panic. And if you are unsure whether your income puts you in scope, or which software suits your situation, get professional advice now rather than in october when the pressure is on.

— Chris

How Cwabc helps landlords with MTD compliance

Cwabc works with landlords across Tonbridge and Kent to set up MTD-compatible software and maintain clean, compliant digital records throughout the year.

Whether you need help choosing between Xero, FreeAgent, or QuickBooks, or you want someone to handle your quarterly reporting and final declaration, Cwabc provides clear, jargon-free support at every stage. The firm’s accounting software setup service is tailored specifically for landlords navigating MTD for the first time. Pricing is upfront, and there are no surprises. Get in touch for a free, no-obligation conversation about your landlord tax compliance needs.

Need help?

If you are ready to talk through your MTD obligations, contact Cwabc for a free, no-obligation conversation. Getting the right support early makes the whole process far simpler.

FAQ

What is Making Tax Digital for landlords?

Making Tax Digital for Income Tax Self Assessment is an HMRC programme requiring unincorporated landlords with qualifying income above £50,000 to keep digital records and submit quarterly updates, replacing the annual Self Assessment return from april 2026.

Does MTD apply to limited company landlords?

No. Limited company landlords pay Corporation Tax, not Income Tax, so MTD for ITSA does not apply to them. They continue submitting corporation tax returns under a separate HMRC process.

What happens if I miss a quarterly MTD deadline?

Each missed submission earns one penalty point. Four points trigger a £200 fine. Points accumulate across missed quarterly updates and final declarations, so consistent late filing becomes costly.

Do I need to buy software to comply with MTD?

Yes. HMRC does not supply free MTD software. Landlords must choose from commercially approved products. Spreadsheets are non-compliant unless connected to HMRC’s systems through bridging software.

Can I get an exemption from Making Tax Digital?

You can apply to HMRC for a digital exclusion exemption on grounds of age, disability, location, or religious belief. HMRC reviews each application individually, so apply well before your compliance date.