Corporation Tax is the tax UK limited companies pay on their taxable profits, collected and administered by HM Revenue and Customs (HMRC). Every UK limited company must register for Corporation Tax, file a Company Tax Return (known as the CT600), and pay any tax owed according to strict deadlines. The rules apply whether your company made a large profit or a modest one. Even dormant companies may face filing obligations if HMRC issues a notice to file. Getting this right from the start saves you from penalties, interest charges, and unnecessary stress later on.

What are the current corporation tax rates and thresholds?

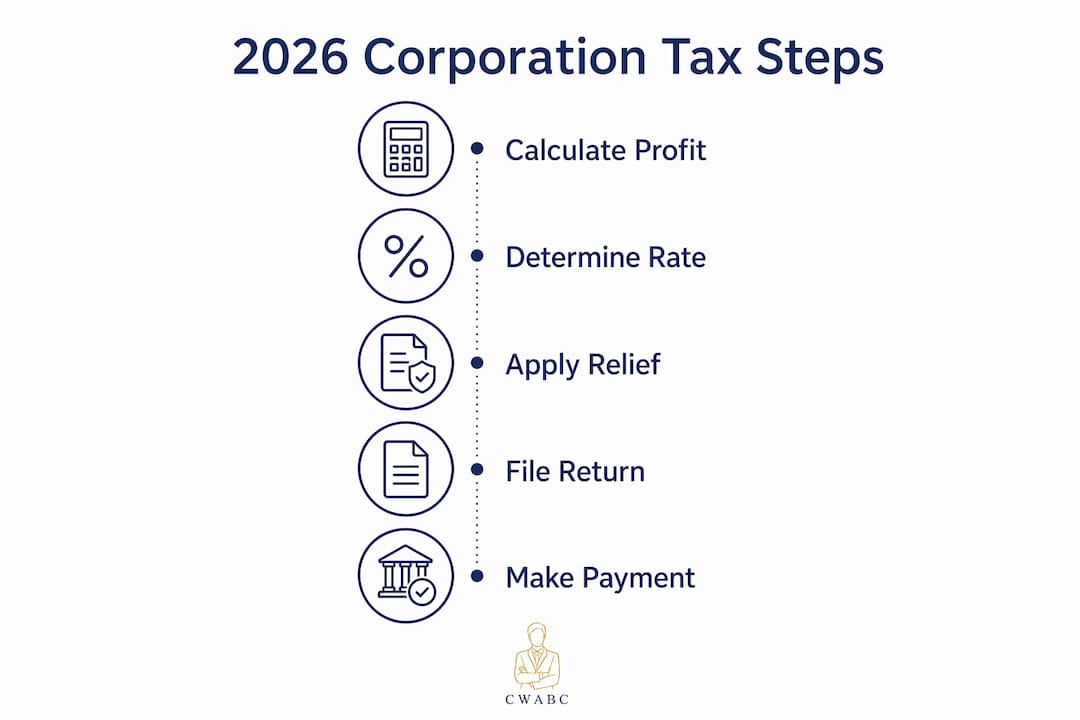

Corporation Tax rates in 2026 follow a two-tier structure, with a sliding scale in between. The rate your company pays depends on how much taxable profit it makes in an accounting period.

The small profits rate and main rate

The small profits rate is 19%, and it applies to companies with taxable profits up to £50,000. The main rate is 25%, and it applies to profits over £250,000. Companies with profits between £50,000 and £250,000 pay an effective rate somewhere between the two, calculated using marginal relief.

Marginal relief reduces your tax bill gradually as profits rise from £50,000 toward £250,000. The relief is calculated using a standard formula set by HMRC, and the result is a smooth increase in your effective rate rather than a sudden jump. This matters because a company with £150,000 in profits does not simply pay 25% on the full amount.

How thresholds change for associated companies

The profit thresholds are divided among associated companies and adjusted for accounting periods shorter than 12 months. If you own or control two companies, each company’s thresholds are halved. A company with a six-month accounting period has its thresholds halved again. This catches many directors off guard, so check your associated company position before assuming the 19% rate applies.

| Taxable profit | Rate applied | Notes |

|---|---|---|

| Up to £50,000 | 19% (small profits rate) | Standard 12-month period, no associated companies |

| £50,001 to £250,000 | 19%–25% (marginal relief) | Effective rate rises gradually across this band |

| Over £250,000 | 25% (main rate) | Full main rate applies |

| Thresholds with 2 associated companies | Halved (£25,000 / £125,000) | Each company uses reduced thresholds |

| Short accounting period (e.g. 6 months) | Thresholds prorated | £25,000 / £125,000 for a 6-month period |

Pro Tip: If your profits sit close to £50,000, making an additional pension contribution or bringing forward a capital purchase before your year end can keep you within the small profits rate. Speak to an accountant before your accounting period closes.

How and when must limited companies file and pay?

Payment is due 9 months and 1 day after the accounting period ends. The CT600 Company Tax Return must be filed within 12 months of the accounting period end. These two deadlines are separate, and the payment deadline comes first. Many directors miss this distinction and end up paying late.

The CT600 filing process step by step

- Register for Corporation Tax with HMRC as soon as your company is incorporated. You must do this within three months of starting to trade.

- Set up a Government Gateway account and link it to your company’s Unique Taxpayer Reference (UTR). HMRC sends your UTR by post after registration.

- Prepare your statutory accounts for the accounting period. These form the basis of your tax computation.

- Complete your tax computation, adjusting accounting profit for disallowable expenses and capital allowances to arrive at taxable profit.

- File the CT600 electronically using approved commercial software or through an accountant. Since 31 march 2026, HMRC’s free CT600 filing service closed permanently. Paper filing is not accepted for most companies.

- Pay your Corporation Tax using the correct 17-character payment reference. This reference is derived from your UTR and accounting period number.

- Keep records of your accounts, tax computations, and supporting documents for at least six years.

Getting the payment reference right

The 17-character payment reference must be copied exactly from your HMRC online account. Using an incorrect or guessed reference risks your payment being misallocated. HMRC will not automatically match a payment made with the wrong reference, and you could face late payment penalties even if the money left your bank account on time.

Penalties for late filing and late payment

Late filing penalties start at £100 one day after the deadline. They escalate to 10% surcharges on unpaid tax after 12 months. Interest also accrues on unpaid tax from the payment due date. The longer you leave it, the more expensive the problem becomes.

Pro Tip: Set a calendar reminder for both deadlines the moment your accounting period ends. The payment deadline arrives three months before the filing deadline, so treat them as two separate events in your diary.

You can find a full breakdown of key dates in the 2026 tax deadline calendar for UK small businesses.

What expenses and allowances reduce your taxable profit?

Taxable profit equals accounting profit adjusted by adding back disallowable expenses and deducting capital allowances. The starting point is always your profit and loss account. From there, you make specific adjustments before arriving at the figure HMRC taxes.

Allowable and disallowable expenses

Understanding which costs qualify is one of the most practical ways to reduce your tax bill legally.

Allowable expenses (reduce your taxable profit):

- Salaries and wages, including director salaries paid through payroll

- Employer National Insurance contributions

- Office rent, utilities, and business rates

- Business travel and mileage at approved rates

- Professional subscriptions and trade memberships

- Accountancy and bookkeeping fees

- Business insurance premiums

- Stock and raw materials used in the business

- Software subscriptions used wholly for business purposes

Disallowable expenses (added back to profit):

- Client entertaining and hospitality

- Depreciation on fixed assets (replaced by capital allowances)

- Fines and penalties

- Personal expenses claimed through the business

- Dividends paid to shareholders

Capital allowances and director salary

Capital allowances replace depreciation for tax purposes. When your company buys equipment, machinery, or vehicles, you cannot deduct the full cost through your profit and loss account in the usual way. Instead, you claim capital allowances, which reduce taxable profit directly. The Annual Investment Allowance (AIA) allows most small companies to deduct the full cost of qualifying plant and machinery in the year of purchase, up to the current limit set by HMRC.

Director salary treatment deserves particular attention. A salary paid through PAYE is an allowable expense for Corporation Tax purposes. This is why many directors pay themselves a modest salary and take the remainder as dividends. Dividends are paid from post-tax profit and are not a deductible expense for the company. Getting this balance right requires accurate payroll records and clear bookkeeping. The bookkeeping FAQs on the Cwabc website cover common questions on record-keeping for exactly this reason.

Good record-keeping is not optional. HMRC can open an enquiry into any return, and you need to be able to substantiate every expense claim with receipts, invoices, and bank statements.

What are the most common Corporation Tax filing mistakes?

Filing errors cost UK limited companies time, money, and unnecessary stress. Most mistakes are avoidable with a little preparation and the right systems in place.

Common mistakes and how to avoid them

- Filing late because the deadline was missed or confused with the payment deadline. Set both dates in your calendar immediately after your accounting period ends.

- Paying late because the payment deadline was treated as the same as the filing deadline. Remember: payment is due three months earlier than the return.

- Using the wrong payment reference. A guessed or outdated reference causes misallocation. Always copy the exact 17-character reference from your HMRC online account.

- Attempting to use HMRC’s free filing tool. That service closed on 31 march 2026. Companies that try to use it will be unable to file and may miss their deadline.

- Claiming disallowable expenses such as client entertaining or personal costs, which HMRC will add back during an enquiry.

- Not filing when profits are nil. UK companies must file a tax return if HMRC issues a notice to file, even if the company made no profit or was dormant. Many directors wrongly assume zero profit means no obligation.

- Inaccurate tax computations caused by poor bookkeeping throughout the year. Errors in your accounts feed directly into errors on your CT600.

- Ignoring associated company rules. Directors who run more than one company often apply the wrong thresholds and end up underpaying tax.

Pro Tip: Reconcile your bank accounts and categorise all transactions monthly rather than leaving it until year end. A tidy set of records at year end makes the tax computation straightforward and reduces the risk of errors.

Corporation Tax compliance is integrated with your statutory accounts, PAYE, and VAT. An error in one area tends to create problems in others. Treating these as separate tasks rather than a connected system is one of the most common mistakes small business directors make. A good small business tax guide can help you see how these obligations fit together.

Key takeaways

Corporation Tax is a mandatory obligation for every UK limited company, and getting the rates, deadlines, and expense claims right from the start is the most reliable way to stay compliant and avoid penalties.

| Point | Details |

|---|---|

| Two-tier rate structure | Pay 19% on profits up to £50,000 and 25% on profits over £250,000, with marginal relief in between. |

| Payment before filing | Corporation Tax is due 9 months and 1 day after the period ends, three months before the CT600 filing deadline. |

| Free filing tool closed | HMRC’s free CT600 service closed 31 march 2026; use approved commercial software or an accountant to file. |

| Expenses reduce taxable profit | Allowable expenses and capital allowances reduce the profit figure HMRC taxes, so accurate records matter. |

| File even with no profit | HMRC requires a return if it issues a notice to file, regardless of whether the company made any profit. |

What I have learned from helping directors get this right

Chris’s perspective on Corporation Tax compliance for limited companies.

The directors I work with most often are not confused about whether they owe Corporation Tax. They are confused about the timing. The payment deadline catches people out every single year, and it is entirely understandable. Most people assume you pay when you file. You do not. By the time the CT600 is due, the tax should already have been paid. If you have not set aside the money throughout the year, that gap becomes a real problem.

The second thing I see regularly is directors treating bookkeeping as a year-end task. When records are left until the last minute, the tax computation is rushed, expenses get missed or miscategorised, and the whole process becomes far more stressful than it needs to be. Monthly bookkeeping is not just good practice. It is the foundation that makes everything else, including your Corporation Tax return, straightforward.

The closure of HMRC’s free CT600 filing tool in march 2026 has changed the landscape for smaller companies who previously filed themselves. If you were using that tool, you now need either approved commercial software or professional support. This is not a bad thing. Approved software tends to produce more accurate returns and flags common errors before submission.

One detail that surprises many directors is the payment reference. It is 17 characters long, derived from your UTR and accounting period. If you type it incorrectly or use an old reference from a previous year, your payment sits unallocated and HMRC treats it as unpaid. That leads to penalty notices even when you paid on time. Copy it exactly, every time.

My honest advice is to treat your Corporation Tax obligations as a year-round process, not an annual event. Keep your records tidy, set your deadlines in advance, and get professional support if any part of the process feels unclear. The CT600 filing process does not have to be stressful when you know what to expect.

— Chris

How Cwabc helps limited companies with Corporation Tax

Running a limited company means staying on top of filing deadlines, tax computations, and ever-changing HMRC requirements. That is a lot to manage alongside actually running your business.

Cwabc supports limited company directors in Tonbridge and across Kent with Corporation Tax filing, bookkeeping, and payroll. The team handles CT600 preparation, tax computations, and HMRC correspondence, using clear, upfront pricing with no jargon. Whether you need help setting up accounting software to keep your records compliant, or you want a professional to manage your company tax return from start to finish, Cwabc offers the practical support that keeps your company compliant and your finances organised.

FAQ

What is Corporation Tax and who pays it?

Corporation Tax is the tax UK limited companies pay on their taxable profits, administered by HMRC. All UK limited companies must register, file a CT600, and pay any tax owed each accounting period.

When is Corporation Tax due?

Payment is due 9 months and 1 day after the accounting period ends. The CT600 Company Tax Return must be filed within 12 months of the accounting period end.

What are the Corporation Tax rates in 2026?

The small profits rate is 19% for profits up to £50,000. The main rate is 25% for profits over £250,000. Marginal relief applies to profits between these two figures.

Do I need to file if my company made no profit?

Yes. If HMRC issues a notice to file, you must submit a CT600 even if your company made no profit or was dormant during the accounting period.

How do I file a CT600 now that HMRC’s free tool has closed?

HMRC’s free CT600 filing service closed permanently on 31 march 2026. You must now use approved commercial software or engage an accountant to file your return electronically.

Need help?

If you have questions about your company’s Corporation Tax obligations or want support with filing your CT600, Cwabc is here to help. Get in touch for a free, no-obligation conversation about your company accounts and tax compliance.