Running a small business in the UK means tax is never far from your mind. The good news is there are plenty of ways to reduce your tax bill legally as a small business owner, without cutting corners or falling foul of HMRC. This guide walks you through the practical steps: choosing the right business structure, claiming every allowable deduction, keeping records that hold up to scrutiny, and using pension contributions and capital allowances to lower your taxable profit. Whether you are a sole trader or a limited company director, these strategies are grounded in compliance and built to last.

Table of Contents

- Key takeaways

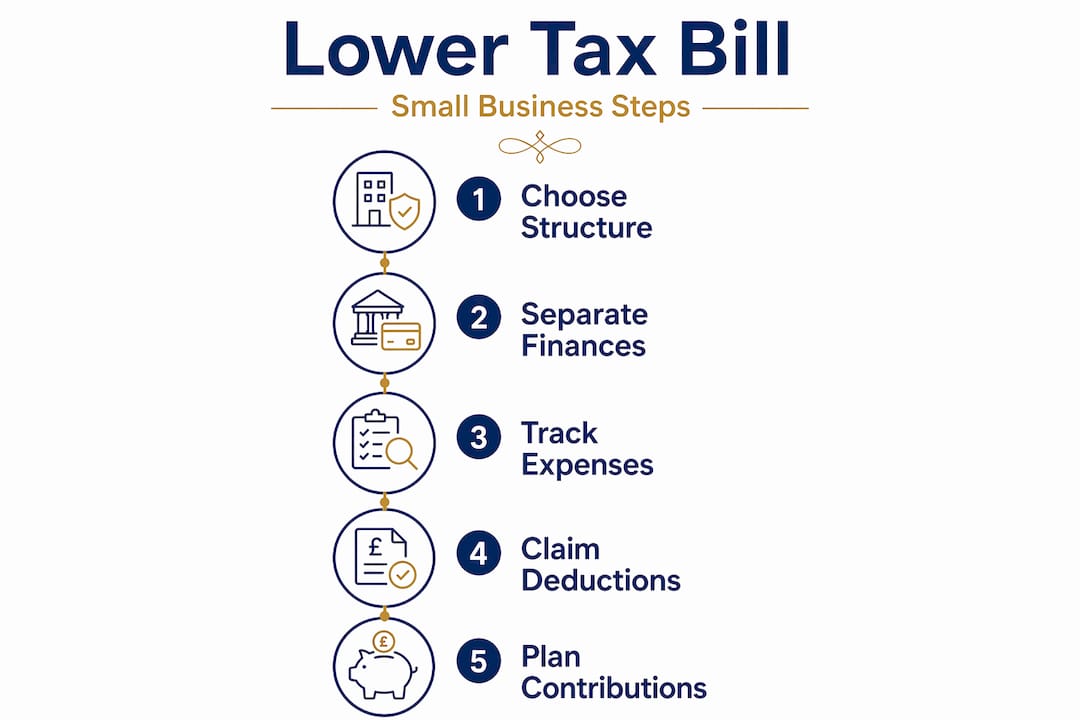

- How to reduce your tax bill legally as a small business

- Your business structure and finances

- Maximising your deductions and credits

- Tax planning and record-keeping that actually works

- Pension contributions and capital allowances

- Compliance: what to avoid

- My honest take on tax strategy for small businesses

- How Cwabc can help you pay less tax, legally

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Structure matters from day one | Your business structure directly affects your tax rate, so choose it with tax efficiency in mind. |

| Claim every allowable expense | Office costs, utilities, equipment, and home office use are all deductible if properly recorded. |

| Records protect your deductions | Accurate bookkeeping is what stands between you and a rejected claim or an HMRC audit. |

| Pension contributions reduce profit | Paying into a pension lowers your taxable income while building long-term financial security. |

| Compliance is your strongest defence | Staying within the rules protects your reputation and keeps costly penalties off the table. |

How to reduce your tax bill legally as a small business

The starting point for any effective tax strategy is understanding what you are working with. Many small business owners pay more tax than they need to, not because they are doing anything wrong, but because they have not set things up in a way that makes the most of what HMRC allows.

There are three broad areas where legal savings are most commonly missed:

- Claiming deductions you are entitled to but have not documented properly

- Being in the wrong business structure for your income level

- Leaving tax planning until January, when the tax year is already closed

Good tax management is not about finding loopholes. It is about knowing the rules well enough to use them fully. The strategies in this guide are all within HMRC’s guidelines and are used by thousands of UK small businesses every year.

Your business structure and finances

Before you claim a single deduction, your foundation needs to be solid. That means two things: the right business structure and clean financial separation.

In the UK, most small businesses operate as sole traders, partnerships, or limited companies. Each carries different tax implications.

- Sole trader: You pay Income Tax and National Insurance on your profits. Simple to set up, but you pay tax at your marginal rate, which rises quickly as profits grow.

- Limited company: The company pays Corporation Tax (currently 19% to 25% depending on profits). You can draw a salary and dividends, which can be more tax-efficient at higher income levels.

- Partnership: Profits are split between partners and taxed individually, which can spread the tax burden.

Strategic structure selection is one of the most powerful and underused tools for reducing your overall tax burden. Many sole traders earning above £30,000 in profit would pay less tax as a limited company, but they have never run the numbers.

Once your structure is right, separate your finances. Open a dedicated business bank account and use it exclusively for business transactions. This is not just good practice. Dedicated business accounts are the single most practical step you can take to maximise deductions and stay compliant. Without clear separation, you risk losing legitimate claims because you cannot prove an expense was for business use.

Pro Tip: If you are a sole trader and have not opened a separate business account yet, do it this week. It takes under an hour and will save you significant time and stress at the end of the tax year.

Maximising your deductions and credits

This is where most of the day-to-day tax saving happens. The more legitimate expenses you claim, the lower your taxable profit. Here is a structured way to think about it.

The main categories of allowable expenses

- Office costs: Rent, utilities, phone bills, and broadband used for business purposes are fully deductible expenses for most small businesses.

- Employee costs: Salaries, employer National Insurance contributions, and pension contributions you make on behalf of staff all reduce your taxable profit.

- Equipment and technology: Computers, printers, software subscriptions, and tools used in the business can be claimed. In many cases, the full cost can be written off in the year of purchase.

- Advertising and marketing: Website costs, social media advertising, print materials, and PR all qualify.

- Insurance: Business insurance premiums are deductible.

- Travel: Business mileage, train tickets, and accommodation for business trips can be claimed. Keep a mileage log if you use your own vehicle.

Home office deductions

If you work from home, you can claim a proportion of your household costs. HMRC allows either a flat rate based on hours worked at home or a calculation based on the actual proportion of your home used for business. The flat rate is simpler. The actual cost method can be more generous if you use a dedicated room.

| Deduction type | Method | Best suited for |

|---|---|---|

| Home office flat rate | Fixed amount per month based on hours | Occasional home workers |

| Actual cost proportion | % of rent, utilities, broadband | Dedicated home office users |

| Startup costs | Claim up to a set threshold immediately | New businesses in first year |

For new businesses, HMRC allows you to claim certain pre-trading expenses. Startup costs up to a threshold can be deducted immediately, with any excess spread over a longer period. Keep all receipts from before you officially started trading.

You can find a detailed breakdown of what counts as a claimable expense in Cwabc’s guide to business expenses for sole traders.

Pro Tip: Do not wait until the end of the tax year to categorise your expenses. Set aside 20 minutes each week to log receipts and reconcile your accounts. This habit alone prevents the last-minute scramble that causes missed claims.

Tax planning and record-keeping that actually works

Knowing what you can claim is only half the job. The other half is being able to prove it. Accurate and thorough records are what allow you to claim deductions confidently and withstand any HMRC enquiry.

Here is what good record-keeping looks like in practice:

- Keep all receipts, digital or paper, for every business purchase. HMRC can ask for evidence going back several years.

- Reconcile your accounts monthly, not annually. Errors are far easier to spot and fix when they are fresh.

- Use bookkeeping software such as Xero, QuickBooks, or FreeAgent to automate categorisation and reduce manual errors. Cwabc has a helpful guide on moving to cloud accounting if you are still working from spreadsheets.

- Track business mileage every time you use your vehicle for work. A simple app or logbook works well.

- Make timely payments. Late estimated tax payments attract penalties that eat into any savings you have made through deductions.

The businesses that get into trouble are almost never the ones doing anything deliberately wrong. They are the ones whose records are too messy to support legitimate claims. Poor bookkeeping is genuinely one of the hidden costs of running a business that most owners do not see until it is too late.

Pro Tip: Set up a simple folder system, digital or physical, with one folder per tax year and subfolders by expense category. Doing this from day one takes minutes. Recreating it at year-end takes days.

Pension contributions and capital allowances

These two strategies are used by experienced business owners to reduce taxable profit significantly, and they are often overlooked by those earlier in their business journey.

Pension contributions

Pension contributions reduce taxable income while building your retirement savings at the same time. For sole traders, contributions to a personal pension are made from post-tax income, but you receive tax relief at your marginal rate. For limited company directors, employer pension contributions made by the company are a deductible business expense, which means the company pays less Corporation Tax.

The practical effect is significant. A limited company director contributing £10,000 into a pension via the company saves Corporation Tax on that amount, and the money grows in a tax-advantaged environment. It is one of the most efficient ways to extract value from a profitable business.

Capital allowances and the Annual Investment Allowance

When you buy equipment, vehicles, or machinery for your business, you generally cannot deduct the full cost as a regular expense. Instead, you claim capital allowances. The Annual Investment Allowance (AIA) allows you to deduct qualifying purchases up to £1 million immediately, rather than spreading the relief over several years.

| Method | How it works | Tax impact |

|---|---|---|

| Capital allowances (standard) | Relief spread over several years | Gradual reduction in taxable profit |

| Annual Investment Allowance (AIA) | Full cost deducted in year of purchase | Immediate reduction in taxable profit |

| Depreciation (accounting) | Spread over asset’s useful life | Not directly tax-deductible |

Timing your purchases matters. If you are close to the end of your accounting year and planning a significant equipment purchase, buying before the year-end rather than after can bring the tax relief forward by a full year.

Compliance: what to avoid

Reducing your tax bill legally means staying well clear of practices that cross the line. The consequences of getting this wrong are serious and long-lasting.

- Never mix personal and business expenses. Mixing personal and business costs can trigger audits, result in fines, and cause you to lose deductions you were legitimately entitled to.

- Avoid aggressive tax schemes. HMRC actively targets arrangements that have no commercial purpose beyond avoiding tax. The penalties can far exceed the original saving.

- File accurately and on time. Errors in your Self Assessment or Corporation Tax return, even honest ones, can attract penalties and enquiries.

- Work with a qualified professional. Consulting a qualified adviser early for structural and deduction planning can significantly enhance your legal tax savings and reduce the risk of costly mistakes.

“Compliance is not a burden. It is the foundation that makes every other tax strategy possible. Without it, your savings are always at risk.”

Approaching your tax obligations with care and structure is not just about avoiding fines. It builds credibility with lenders, investors, and HMRC itself.

My honest take on tax strategy for small businesses

In my experience working with sole traders and small business owners, the biggest tax mistakes are rarely about greed. They are about delay. People put off sorting their records, delay choosing the right structure, and leave tax planning until the self-assessment deadline is days away.

What I have seen consistently is this: the business owners who pay the least tax legally are not the ones chasing clever schemes. They are the ones who set up clean systems early, claim everything they are entitled to, and review their position at least once a year with someone who knows what they are looking at.

I have also seen the other side. A sole trader who had been mixing personal and business spending for three years, facing an HMRC enquiry, trying to reconstruct records from memory. The stress alone was enormous, before any financial consequence.

My honest view is that tax planning is not a year-end activity. It is a year-round habit. Contributing to a pension, timing a capital purchase, choosing the right structure before your profits grow, these are decisions that compound over time. The businesses that get this right do not feel clever about it. They just feel calm.

Approach your taxes the way you approach any other part of your business: with a system, with good information, and without leaving it to the last minute.

— Chris

How Cwabc can help you pay less tax, legally

If this article has made you think “I should probably get this sorted properly,” that is exactly the right instinct.

At Cwabc, we work with sole traders and small business owners across Tonbridge and Kent to put the right systems in place from the start. That means clean bookkeeping, clear expense categorisation, timely submissions, and advice tailored to your specific situation. No jargon, no surprises, and no last-minute panic.

Whether you are just starting out or you have been trading for years and suspect you are missing deductions, our bookkeeping services in Tonbridge are designed to give you confidence in your numbers and compliance in your filings.

You can also explore our bookkeeping FAQs for small businesses to get answers to the questions we hear most often. Or, if you are ready to talk through your situation, get in touch and we will take it from there.

FAQ

What expenses can I deduct as a UK sole trader?

You can deduct costs that are wholly and exclusively for business use, including office rent, utilities, equipment, travel, advertising, and insurance. Keep receipts for everything, as HMRC can request evidence to support your claims.

Is it legal to pay myself a pension to reduce my tax bill?

Yes. Pension contributions are one of the most tax-efficient ways to reduce taxable profit, particularly for limited company directors making employer contributions. Sole traders also receive tax relief on personal pension contributions at their marginal rate.

How does the Annual Investment Allowance work?

The AIA allows you to deduct the full cost of qualifying equipment and machinery purchases in the year you buy them, up to £1 million, rather than spreading the relief over several years. Timing your purchases to fall before your accounting year-end can maximise the benefit.

What happens if I mix personal and business expenses?

Mixing personal and business costs can lead to HMRC enquiries, lost deductions, and financial penalties. Keeping a dedicated business bank account and logging expenses accurately is the simplest way to avoid this problem entirely.

When should I consider switching from sole trader to limited company?

Many accountants suggest reviewing your structure once your profits consistently exceed around £30,000 to £35,000 per year. At that level, the tax advantages of a limited company structure often outweigh the additional administrative requirements.