A small business tax payment budget plan is a structured method for setting aside funds regularly to meet HMRC obligations on time and avoid financial stress. Think of it as giving your tax bill its own savings pot, separate from the money you use to run your business day to day. Without a plan, tax deadlines arrive faster than expected, and the cash simply is not there. This guide walks you through the key tax obligations you need to budget for, how much to set aside based on your income, and the practical steps to build a plan that keeps you compliant and calm throughout 2026.

What are the key tax payment obligations small businesses must budget for?

Your small business tax payment budget plan only works if you know exactly what you are budgeting for. UK small businesses face several distinct tax obligations, each with its own deadlines and payment rules. Getting clear on these early is the foundation of any solid annual tax planning guide.

The main taxes to plan around are:

- Income Tax on your trading profits, paid through Self Assessment

- Class 2 and Class 4 National Insurance Contributions (NICs), which apply to self-employed sole traders

- VAT, if your taxable turnover exceeds the current registration threshold (£90,000 as of 2026), payable quarterly or monthly depending on your VAT scheme

- Corporation Tax, if you trade through a limited company, due nine months and one day after your accounting year end

For sole traders and partnerships, Self Assessment payments follow a specific schedule. HMRC requires two payments on account each year: the first by 31 january and the second by 31 july. A balancing payment is then due the following 31 january if your actual tax bill exceeds the payments already made. This cycle catches many new business owners off guard in their second year of trading.

Small businesses expecting to owe £1,000 or more in tax annually must make estimated payments to avoid penalties. Missing these deadlines triggers interest charges and late payment penalties from HMRC, which add up quickly.

To stay on the right side of HMRC, you can use the safe harbour approach. This means paying either 90% of your current year’s tax liability or 100% of the previous year’s tax bill, whichever is lower. Safe harbour rules protect you from underpayment penalties even if your income rises unexpectedly during the year. For higher earners, the threshold rises to 110% of the prior year’s liability.

Understanding your full tax obligations before you start budgeting prevents nasty surprises and keeps your planning grounded in reality.

How much should you set aside for tax payments?

The most practical rule for budgeting for tax payments is to reserve a percentage of your net profit every time money comes in. The exact percentage depends on your income level.

A widely used guide for sole traders and small business owners is:

- Lower income (below approximately £30,000 net profit): set aside 20–25% of net profit

- Mid-range income (approximately £30,000–£80,000 net profit): set aside 25–30% of net profit for tax

- Higher income (above approximately £80,000 net profit): set aside 30–35%, accounting for the higher Income Tax rate and additional NICs

These brackets exist because the UK tax system is progressive. As your profit rises, a larger slice falls into the 40% higher rate band, and your Class 4 NIC liability increases too. Setting aside a higher percentage early means you are never scrambling when the bill arrives.

Several factors shift these percentages up or down. Allowable business expenses reduce your taxable profit, so a business with high legitimate costs will owe less than the raw percentage suggests. The Annual Investment Allowance, capital allowances, and the Trading Allowance all affect the final figure. This is why tax planning differs from tax preparation: preparation is filing your return, while planning is the year-round process of making decisions that reduce your bill before it is calculated.

Pro Tip: Open a dedicated savings account and label it “Tax.” Every time a client pays you, transfer your chosen percentage immediately. Treat this transfer as non-negotiable, the same way you would treat rent or a supplier invoice.

A practical example: if you invoice £5,000 in a month and your net profit after expenses is £3,500, transferring 28% gives you £980 set aside for tax. Do this consistently and the january payment on account becomes a non-event rather than a crisis.

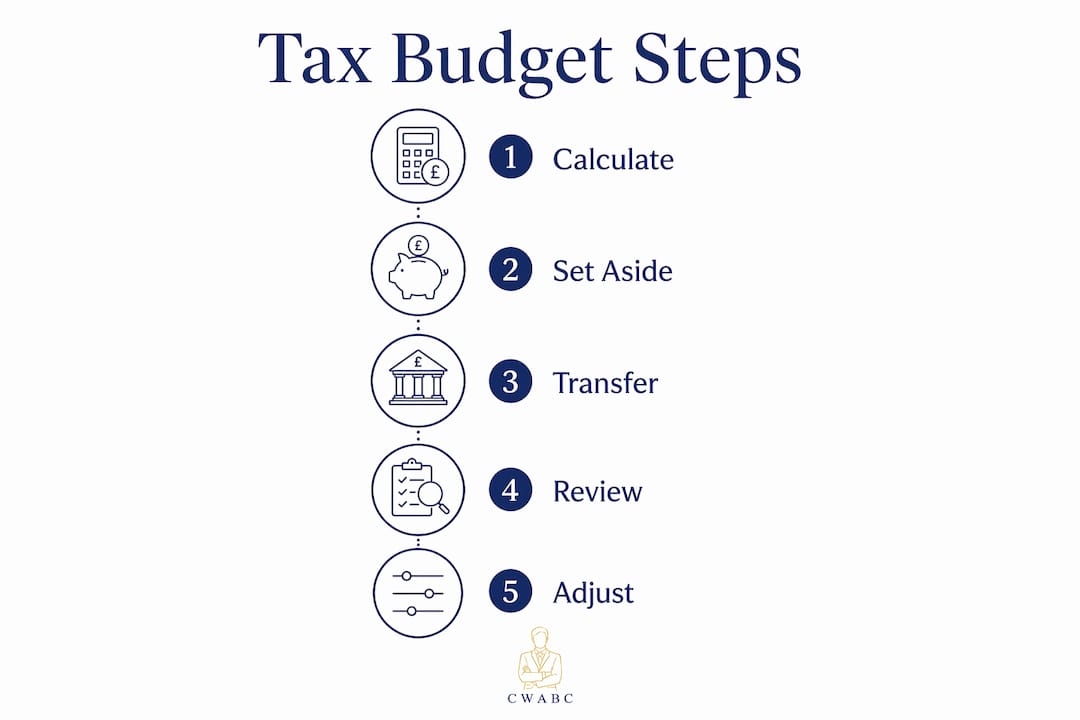

Practical steps to set up and maintain a tax budget plan

Building a tax budget plan does not require complex software or an accountant on speed dial from day one. It requires a clear system and the discipline to follow it. Here is how to set one up properly.

-

Open a separate tax savings account. Use a business savings account or a second current account specifically for tax funds. Never mix this money with your operating account. The separation removes the temptation to spend funds that are not truly yours.

-

Set a fixed transfer percentage. Based on your income bracket, choose your percentage (25–30% is a safe starting point for most sole traders). Set up a standing order or automatic transfer to move that amount every time a payment clears. Automatic transfers remove the decision from your hands and eliminate the risk of spending tax money by mistake.

-

Make payments on time. HMRC accepts payment by direct debit, online banking, or through your Government Gateway account. You can also pay more frequently than quarterly if that suits your cash flow. Monthly payments are permitted provided the total due is covered by each quarterly deadline.

-

Review your income every quarter. Proactive business owners review income quarterly to adjust their estimated payments and check whether their set-aside percentage still reflects reality. If you have had a strong quarter, increase your transfer rate. If income has dropped, recalculate to avoid over-saving.

-

Keep accurate records throughout the year. Good bookkeeping is not just about compliance. It gives you the numbers you need to make accurate estimates. Bookkeeping prevents tax stress precisely because it keeps your profit figures current and your estimates grounded in real data.

-

Adjust for seasonal income. If your business earns more in certain months, such as a retail business peaking at Christmas or a landscaping business quieter in winter, your fixed percentage approach still works. You simply save more in high-income months and draw on the tax account in quieter periods.

The table below shows how different income levels translate into practical monthly transfer amounts, assuming a 28% set-aside rate on net profit.

| Monthly net profit | Set-aside rate | Monthly transfer to tax account |

|---|---|---|

| £1,500 | 25% | £375 |

| £3,000 | 28% | £840 |

| £5,000 | 30% | £1,500 |

| £8,000 | 33% | £2,640 |

Pro Tip: At the end of each tax year, any surplus in your tax account above what HMRC requires is yours to keep or reinvest. Many business owners find this surplus becomes a useful buffer or a small business investment fund.

Common mistakes in budgeting for tax payments and how to avoid them

Even well-intentioned business owners fall into predictable traps when managing tax payments. Knowing these pitfalls in advance is half the battle.

-

Underestimating income. If your business grows faster than expected, your tax bill grows with it. Basing your payments on last year’s lower income leaves a gap. Review your figures quarterly rather than annually.

-

Mixing tax funds with operating money. This is the most common and costly mistake. When tax money sits in your main account, it gets spent. A separate account makes the boundary clear and protects you from an unpleasant shock in january.

-

Waiting until the deadline to start saving. Starting to save for a january payment in december is too late for most businesses. The habit of saving from every payment, starting from your first invoice, is what makes the system work.

-

Ignoring allowable deductions. Failing to use available deductions costs small businesses real money. Expenses like home office costs, mileage, professional subscriptions, and equipment purchases all reduce your taxable profit. Claiming them accurately means your tax bill is lower than a rough estimate suggests, and your set-aside percentage can be refined accordingly.

-

Skipping professional advice when things get complex. If your income rises significantly, you take on employees, or you consider incorporating, the tax picture changes substantially. Knowing when to involve a tax professional saves money in the long run.

“Tax planning is not a once-a-year event. It is a year-round discipline that protects your cash flow and keeps your business on solid ground.” — Cwabc

Frequent reviews and updates to your budget plan are not optional extras. They are the mechanism that keeps your plan accurate as your business evolves.

Which tax budgeting method suits your business best?

Not every business suits the same approach to saving for tax. The right method depends on how predictable your income is and how comfortable you are with complexity.

| Method | How it works | Best for | Complexity | Penalty risk |

|---|---|---|---|---|

| Fixed percentage per payment | Transfer a set % every time money arrives | Freelancers, sole traders with variable income | Low | Low if % is set correctly |

| Monthly saving | Transfer a fixed amount each month | Businesses with steady monthly income | Low | Medium if income rises unexpectedly |

| Quarterly lump sum | Save up and pay HMRC each quarter | Businesses with strong cash reserves | Medium | Medium if cash flow dips |

| Safe harbour method | Pay 100% of prior year’s tax bill | Businesses with growing income | Low | Very low |

| Annualised income method | Base each payment on actual income that quarter | Seasonal businesses | High | Low if calculated correctly |

The safe harbour method is the simplest protection against penalties. You pay what you owed last year, regardless of whether this year’s income is higher or lower. The downside is a potential large balancing payment in january if your income has grown significantly.

The annualised income method suits seasonal businesses far better. It bases each payment on the actual income earned in that quarter rather than a fixed annual estimate. A holiday lettings business, for example, earns most of its income in summer. Paying tax based on actual quarterly income avoids overpaying in winter and underpaying in summer.

For most sole traders starting out, the fixed percentage per payment method is the most practical. It requires no complex calculations and builds the saving habit from day one. As your business grows and your income becomes more predictable, you can shift to the safe harbour or annualised method for greater accuracy.

Key takeaways

A consistent small business tax payment budget plan, built around a dedicated savings account and a fixed percentage of net profit, is the most reliable way to meet HMRC deadlines without financial stress.

| Point | Details |

|---|---|

| Know your obligations | Budget for Income Tax, NICs, VAT, and Corporation Tax based on your business structure. |

| Set aside the right percentage | Reserve 25–30% of net profit for most income levels, rising to 30–35% for higher earners. |

| Automate your saving | Transfer your chosen percentage to a dedicated tax account with every payment received. |

| Review quarterly | Adjust your estimates every three months to reflect actual income and avoid underpayment. |

| Choose the right method | Use the safe harbour method for simplicity or the annualised income method for seasonal businesses. |

Why I think tax budgeting is the most underrated business habit

After working with sole traders and small business owners across Kent and beyond, the pattern I see most often is this: the businesses that struggle with tax are not the ones with complicated finances. They are the ones that never built a saving habit in the first place.

Tax stress is almost always a cash flow problem in disguise. The bill itself is not the shock. The shock is discovering the money is not there. I have seen profitable businesses genuinely panicked by a january Self Assessment bill that was entirely predictable six months earlier. The profit was real. The planning was not.

What I find works best is treating your tax account the way you treat your rent. You do not debate whether to pay it. You do not dip into it for a quiet month. It is simply off-limits. That psychological shift, from “I will sort it later” to “this money is already spoken for,” changes everything.

Automation is the most powerful tool here. When the transfer happens automatically, you never feel the loss. The money moves before you have a chance to spend it. Business owners who automate this process consistently tell me they forget the tax account exists until january, and then they are pleasantly surprised to find exactly what they need sitting there.

Viewing tax payments as a sign of business health rather than a burden also matters more than people realise. A tax bill means you made a profit. That is worth celebrating, not dreading. The goal of a good budget plan is not to minimise the feeling of paying tax. It is to make the payment so unremarkable that it barely registers.

— Chris

Need help with your tax payment planning?

Getting your tax budget right from the start saves time, money, and a great deal of stress. Cwabc supports sole traders and small business owners across Tonbridge and Kent with practical bookkeeping, Self Assessment, VAT, and Making Tax Digital preparation.

Whether you need help setting up your first tax savings system, catching up on records, or preparing for Making Tax Digital in 2026, Cwabc offers clear, upfront pricing and no-jargon support. The team also provides expert bookkeeping services in Tonbridge to keep your finances organised and your tax estimates accurate year-round. For a free, no-obligation conversation, visit the Cwabc contact page and get in touch today.

FAQ

What is a small business tax payment budget plan?

A small business tax payment budget plan is a structured system for setting aside a percentage of income regularly to cover HMRC tax obligations, including Income Tax, NICs, and VAT, before each deadline arrives.

How much should a sole trader set aside for tax in the UK?

Most sole traders should reserve 25–30% of net profit for tax, rising to 30–35% for higher earners. The exact figure depends on your income level, allowable expenses, and whether you are VAT-registered.

What happens if I miss an HMRC payment on account?

HMRC charges interest on late payments and may issue a penalty notice. Paying at least 90% of your current year’s liability, or 100% of the previous year’s bill, protects you under safe harbour rules.

Can I pay my tax bill monthly instead of quarterly?

Yes. HMRC permits more frequent payments than the standard quarterly schedule, provided the total due is covered by each quarterly deadline. Monthly payments can make cash flow easier to manage for businesses with steady income.

When should I get professional help with tax budgeting?

Seek professional support when your income rises significantly, you consider incorporating, or your tax affairs become complex. A licensed bookkeeper or accountant can identify deductions you may be missing and help you reduce your tax bill legally.