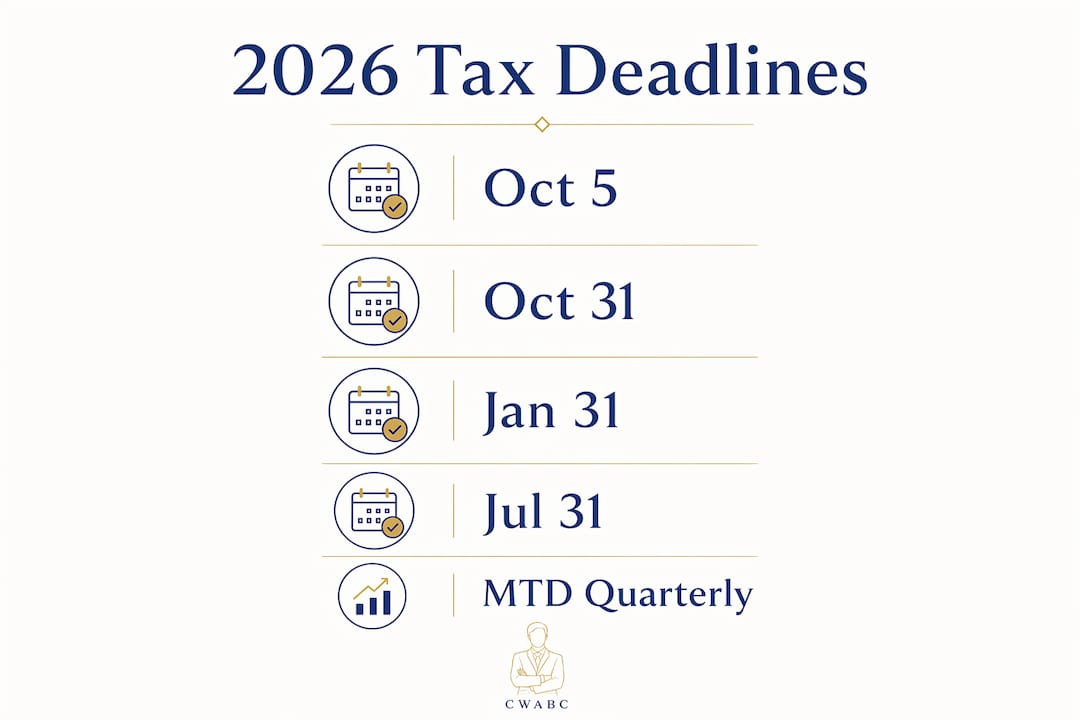

Sole trader tax deadlines are the official dates by which self-employed individuals in the UK must register with HMRC, file their Self Assessment tax return, and pay any tax owed. Miss one of these dates and you face automatic penalties, interest charges, and the risk of an HMRC enquiry. The core dates are 5 October for registration, 31 October for paper returns, and 31 January for online filing and payment. From April 2026, Making Tax Digital for Income Tax (MTD ITSA) adds quarterly reporting obligations for higher earners. Understanding these dates from the start of your trading life is the single most effective way to stay in control of your finances.

What are the main tax deadlines sole traders need to know?

Sole trader tax deadlines explained simply: they follow a fixed annual cycle tied to the UK tax year, which runs from 6 April to 5 April the following year. Every deadline below applies to that cycle, and missing any one of them triggers consequences that compound quickly.

The key dates at a glance

| Deadline | Date | What it covers |

|---|---|---|

| Register for Self Assessment | 5 October | New sole traders must notify HMRC by this date after the tax year they first traded |

| Paper tax return | 31 October | Submit your completed paper Self Assessment return to HMRC |

| Online tax return and payment | 31 January | File your return online and pay all tax owed for the previous tax year |

| First payment on account | 31 January | Pay 50% of your estimated current year tax bill alongside the balancing payment |

| Second payment on account | 31 July | Pay the remaining 50% of your estimated current year tax bill |

The registration deadline is the one most new sole traders overlook. New sole traders must register by 5 October following the end of the tax year in which they first traded. For the 2025/26 tax year, that means registering by 5 October 2026. Miss this date and you risk a late registration penalty, even if you owe no tax at all.

The 31 January deadline is the most significant date in the calendar. It covers three things at once: your online Self Assessment return, your balancing payment for the previous year, and your first payment on account for the current year. For the 2025/26 tax year, all three fall due on 31 January 2027. That is a lot of financial activity concentrated on one date, which is why planning ahead matters so much.

Understanding payments on account

Payments on account are two equal instalments, each covering 50% of your previous year’s tax bill. They apply when your tax due exceeds £1,000 in a tax year. This catches many sole traders off guard in their second year of trading, when they suddenly face paying 150% of their expected bill in January. That is the balancing payment for year one plus the first payment on account for year two, all at once.

Pro Tip: Set aside roughly 25 to 30% of every payment you receive throughout the year. This covers Income Tax, National Insurance, and your payments on account without any last-minute scramble.

The paper return deadline of 31 October is earlier than most people realise. If you miss it, HMRC automatically moves you to the online filing route with the 31 January deadline. Most sole traders file online anyway, but if you rely on an accountant to submit a paper return, that October date is non-negotiable.

How does Making Tax Digital affect sole trader deadlines?

Making Tax Digital for Income Tax (MTD ITSA) is HMRC’s programme to move Self Assessment reporting onto digital platforms, requiring quarterly updates rather than a single annual return. It does not replace the 31 January deadline. It adds to it.

MTD ITSA started on 6 April 2026 for sole traders with gross income over £50,000. The threshold drops to £30,000 in April 2027 and to £20,000 in April 2028. This phased rollout means that two sole traders with similar businesses can have different compliance start dates depending on their income level, which makes planning for MTD genuinely complicated.

Under MTD ITSA, quarterly updates are due on 7 August, 7 November, 7 February, and 7 May. These are digital submissions of your income and expenses for each quarter, sent directly to HMRC via compatible software. They are not tax payments. They are reporting updates. The year-end Self Assessment deadline remains 31 January, unchanged.

Here is what MTD ITSA means in practice for your workflow:

- You need HMRC-compatible software such as Xero, FreeAgent, or QuickBooks to submit quarterly updates

- Your records must be kept digitally from the start of the tax year in which MTD applies to you

- A final end-of-year submission consolidates your quarterly updates and confirms your tax position

- New businesses generally join MTD from their third tax year of trading, once HMRC can confirm their gross receipts from a submitted return

“MTD ITSA’s phased approach based on gross business receipts leads to different start dates for nominally similar sole traders, complicating compliance planning.” — KPMG UK

Sole traders within MTD ITSA should prepare for digital record-keeping well in advance, typically during the late winter months before the 6 April start date. Waiting until April to set up your software and migrate your records is a recipe for missed quarterly deadlines. You can find a full breakdown of the compliance requirements in this MTD ITSA guide for sole traders.

Pro Tip: Check your gross income from your most recent Self Assessment return. If it is approaching £50,000, start setting up MTD-compatible software now, not when HMRC writes to you.

What penalties and risks come from missing deadlines?

Missing a sole trader tax deadline is not a minor administrative slip. HMRC operates an automatic penalty system that escalates the longer a return or payment remains outstanding.

The penalty structure for late filing works like this:

- Immediate £100 penalty on the day after the 31 January deadline, regardless of whether you owe any tax

- Daily penalties of £10 for up to 90 days, adding up to a maximum of £900, once the return is three months late

- A further 5% of the tax due at six months, with a minimum charge of £300

- Another 5% of the tax due at twelve months, again with a minimum of £300

Penalties for missing the 31 January deadline start at an automatic £100. This means you can receive a £100 fine even if your tax bill is zero. That is a detail many sole traders find surprising and frustrating in equal measure.

Late payment carries its own separate charges. Interest accrues on unpaid tax from the day after the deadline. HMRC also applies surcharges of 5% on tax unpaid at 30 days, six months, and twelve months after the payment deadline. These charges stack on top of any filing penalties, so a single missed deadline can generate several overlapping charges.

Failure to register on time can also result in a penalty, even when no tax is owed. HMRC may waive this penalty if you have a reasonable excuse and register promptly once you realise the error. Reasonable excuses include serious illness, bereavement, or technical failures on HMRC’s own systems. “I forgot” or “I was busy” do not qualify.

Record keeping is your best protection against an HMRC enquiry. Sole traders must keep records for at least five years after the 31 January filing deadline for the relevant tax year. HMRC can investigate returns up to 20 years back in cases of deliberate non-compliance. Keeping clean, organised records throughout the year is far less stressful than reconstructing them under investigation. HMRC’s Self-employment pages also require consistency between your business accounts and your Self Assessment figures. A trial balance reconciliation before submission is standard practice and significantly reduces the risk of triggering an enquiry.

How can sole traders prepare to meet tax deadlines?

Preparation is the difference between a calm January and a chaotic one. The sole traders who consistently meet their deadlines are not necessarily the most financially sophisticated. They are simply the most organised.

- Register early. Do not wait until October to notify HMRC. Register as soon as you start trading. This gives you time to set up your records properly and understand what you owe before the filing deadline arrives.

- Keep records throughout the year. Whether you use a spreadsheet, a dedicated app, or accounting software, update your records weekly. Chasing receipts and invoices in January is avoidable stress.

- Use MTD-compatible software. Tools such as Xero, FreeAgent, and QuickBooks all support MTD ITSA submissions. Setting up accounting software in Kent or your local area early means your quarterly updates are largely automated.

- Set aside tax regularly. A separate savings account for tax is one of the simplest and most effective habits a sole trader can adopt. Aim to transfer a fixed percentage of every payment received, before you spend anything else.

- Know your payments on account. If your tax bill exceeded £1,000 last year, you are already making payments on account. Factor both the January and July payments into your cash flow planning for the year ahead.

- Stay informed about MTD changes. The income thresholds for MTD ITSA are dropping each year. Check whether you will be drawn into the scheme in 2027 or 2028 and plan accordingly. This guide on businesses affected by MTD is a useful starting point.

- Consider professional support. A licensed bookkeeper or accountant takes the deadline pressure off your plate entirely. They also spot errors before submission, reducing your enquiry risk.

Pro Tip: Diarise all five key dates at the start of each tax year: 5 October, 31 October, 31 January, 31 July, and your four MTD quarterly deadlines if applicable. Set a reminder two months before each one.

One common pitfall is assuming that because you have filed your return, you have also paid your tax. Filing and payment are separate actions. You can submit your return on time and still receive a late payment penalty if the funds do not reach HMRC by 31 January. Always confirm both are complete.

Another mistake is underestimating the January bill. If you are in your second year of trading and payments on account apply, your January payment will be larger than you expect. Planning your cash flow around Self Assessment deadlines from October onwards gives you the breathing room to manage it calmly.

Key takeaways

Meeting sole trader tax deadlines requires knowing five fixed dates, understanding how payments on account work, and preparing your records and software well before each deadline arrives.

| Point | Details |

|---|---|

| Five core dates | 5 October, 31 October, 31 January, 31 July, and MTD quarterly dates govern your compliance year. |

| Payments on account | Apply when tax exceeds £1,000; January bills are often larger than expected due to overlapping payments. |

| MTD ITSA from April 2026 | Sole traders earning over £50,000 must submit quarterly digital updates via compatible software. |

| Automatic penalties | A £100 fine applies the day after the 31 January deadline, regardless of whether tax is owed. |

| Record keeping | Keep records for at least five years after the filing deadline to protect against HMRC enquiries. |

What I have learned from years of sole trader tax work

Working with sole traders in and around Tonbridge, I see the same patterns every year. The people who struggle most with deadlines are not the ones with complicated finances. They are the ones who started trading without a system and never quite caught up.

The 31 January deadline feels distant in April. By November, it feels urgent. By January, it feels impossible. That gap between “I’ll sort it later” and “I need to sort it now” is where most of the stress lives. The fix is not complicated. It is just consistent. Update your records weekly. Set money aside monthly. Check your registration status before October. Do those three things and the deadline becomes a formality rather than a crisis.

MTD ITSA has changed the conversation I have with clients. The quarterly reporting requirement means that staying on top of your books is no longer optional for higher earners. It is a legal obligation. But here is the thing: sole traders who adopt good digital habits early actually find January easier, not harder. When your quarterly updates are already submitted, the year-end return is mostly a confirmation exercise.

The one thing I would tell every new sole trader is this: register with HMRC as soon as you start trading, not when you think you might owe tax. The registration deadline exists independently of your tax liability. Missing it costs you money and creates an administrative headache that is entirely avoidable.

Cash flow planning around the July payment on account is the other area where I see people caught out. That July date sits in the middle of summer, often when business is quieter and cash reserves are lower. Knowing it is coming and setting aside funds from April onwards makes it manageable. Ignoring it until June does not.

— Chris

How Cwabc helps sole traders stay on top of their deadlines

Staying compliant as a sole trader does not have to mean spending hours on paperwork or worrying about whether you have missed something. Cwabc, based in Tonbridge, works with sole traders across Kent to take the complexity out of tax filing, record keeping, and MTD compliance.

From registering with HMRC at the right time to submitting your Self Assessment return accurately and on time, Cwabc handles the detail so you can focus on your work. The team also supports clients through the transition to Making Tax Digital, including software setup and quarterly submissions. With clear, upfront pricing and no jargon, you always know what you are getting. If you are a sole trader looking for calm, reliable support, visit the sole trader accountant page to find out how Cwabc can help you meet every deadline with confidence.

FAQ

When must a new sole trader register with HMRC?

New sole traders must register for Self Assessment by 5 October following the end of the tax year in which they first traded. For the 2025/26 tax year, the registration deadline is 5 October 2026.

What is the online filing and payment deadline for sole traders?

The online Self Assessment return and all tax payments are due by 31 January following the tax year end. For the 2025/26 tax year, this falls on 31 January 2027.

What happens if you miss the 31 January deadline?

An automatic £100 penalty applies the day after the deadline, with daily £10 charges added after three months and percentage-based penalties at six and twelve months. Interest also accrues separately on any unpaid tax.

Who needs to comply with Making Tax Digital for Income Tax?

Sole traders with gross income over £50,000 must comply with MTD ITSA from 6 April 2026. The threshold drops to £30,000 in 2027 and £20,000 in 2028, bringing more sole traders into the scheme each year.

What are payments on account and when are they due?

Payments on account are two instalments, each equal to 50% of your previous year’s tax bill, due on 31 January and 31 July. They apply when your annual tax liability exceeds £1,000.