Sole trader invoicing rules are the HMRC-defined requirements that determine what every invoice you issue must contain to be legally valid and tax compliant. Getting this right matters more than most sole traders realise. A missing invoice number or an absent legal name can trigger disputes, delay payments, and cause headaches during a Self Assessment review. This guide covers sole trader invoicing rules explained in full, from mandatory fields and VAT differences to record-keeping periods and late payment rights, so you can invoice with confidence and stay on the right side of HMRC.

What must a sole trader include on every invoice?

Every invoice you send must contain specific fields to satisfy HMRC invoicing requirements. These are not suggestions. They are the minimum standard for any sole trader operating in the UK.

Here is what belongs on every invoice you issue:

- Your legal name and trading name. You can invoice under a business name, but your legal name must appear alongside it for HMRC and anti-money laundering compliance. If your business is “Bright Spark Electrical” but your legal name is James Holloway, both must be visible.

- Your address and contact details. Include a business address and at least one contact method, such as an email address or phone number.

- Your customer’s name and address. This confirms who the invoice is directed to and supports any future dispute resolution.

- A unique, sequential invoice number. Each invoice needs its own reference that follows a logical sequence without gaps or repeated numbers.

- Invoice date and supply date. These are two separate pieces of information. The invoice date is when you raised the document. The supply date is when the goods or services were actually delivered.

- A clear description of goods or services. Be specific. “Consultancy services” is vague. “Three hours of social media strategy consultancy on 14 march 2026” is not.

- Itemised amounts and the total owed. Break down each line and show the total clearly.

- Payment terms. State when payment is due, for example “payment due within 14 days of invoice date.”

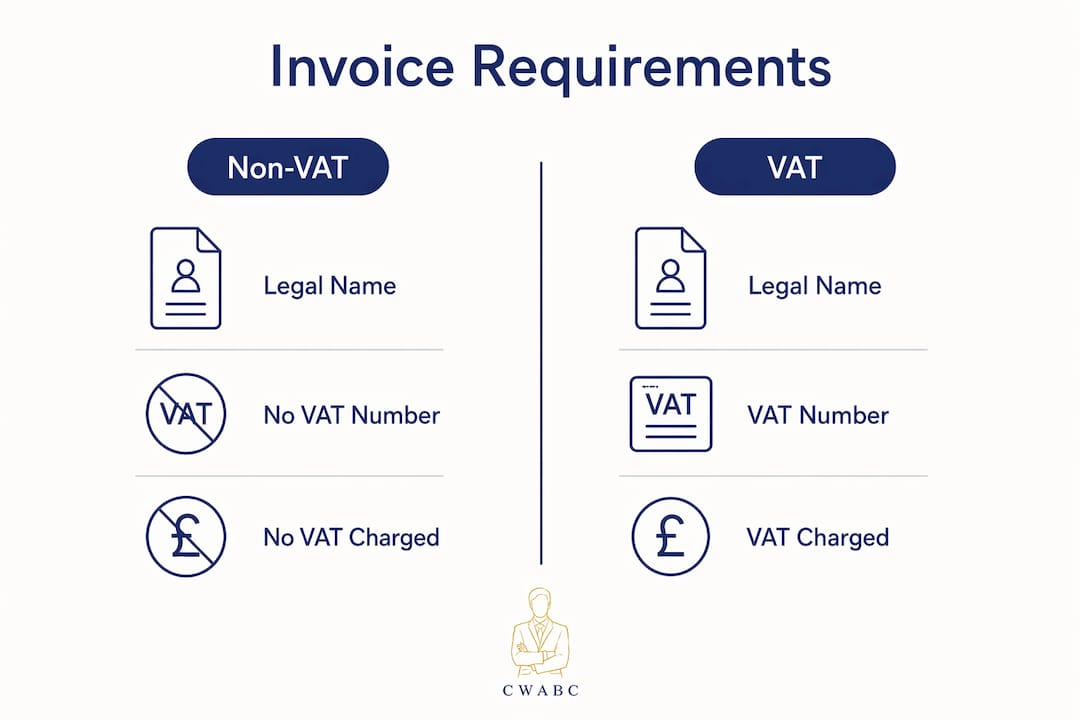

Non-VAT-registered sole traders must not include a VAT number or charge VAT on their invoices. Non-VAT invoices exclude all VAT fields entirely until registration occurs. Adding a VAT charge without being registered is a serious offence.

Pro Tip: Keep a simple invoice template saved with your legal name, trading name, and address pre-filled. This removes the risk of accidentally omitting required details when you are busy.

How do invoicing rules differ for vat-registered sole traders?

VAT registration changes your invoicing obligations significantly. Once you cross the VAT threshold or register voluntarily, your invoices must meet a higher standard. The VAT registration threshold for 2026 is £90,000 in taxable turnover over a rolling 12-month period.

A full VAT invoice must include everything on the standard list above, plus the following additional fields:

- Your VAT registration number

- The VAT rate applied to each line item

- The total VAT amount charged

- The gross total including VAT

- The tax point (also called the time of supply)

The tax point is one of the most misunderstood elements of VAT invoicing. The VAT time of supply can differ from the invoice issue date, and sole traders must manage these dates separately for accurate VAT reporting. For example, if you complete a job on 28 march but raise the invoice on 5 april, the tax point is 28 march. Your VAT return must reflect that date, not the invoice date.

Here is a comparison of what each invoice type requires:

| Field | Non-VAT Invoice | VAT Invoice |

|---|---|---|

| Legal and trading name | Required | Required |

| Invoice number | Required | Required |

| Invoice date and supply date | Required | Required |

| Description and itemised amounts | Required | Required |

| Payment terms | Required | Required |

| VAT registration number | Not applicable | Required |

| VAT rate per line item | Not applicable | Required |

| Total VAT amount | Not applicable | Required |

| Tax point date | Not applicable | Required |

VAT-registered sole traders must issue VAT invoices within 30 days of the tax point when supplying to other VAT-registered customers. Missing this window can cause complications for your customer’s VAT reclaim and may attract scrutiny from HMRC.

If a non-VAT-registered customer requests a VAT invoice, you can issue one on request. There is no obligation to do so proactively, but having a process in place saves time.

Pro Tip: Record your tax point date in a separate column on your invoice log. Do not rely on the invoice date alone. This one habit prevents the most common VAT reporting errors.

What are the best practices for numbering, sending, and record keeping?

Good invoicing habits protect you during audits and make your Self Assessment far less stressful. The three areas that matter most are how you number invoices, how you send them, and how long you keep them.

Invoice numbering done right

Sequential unique numbering supports auditability and statutory compliance. Gaps in your sequence or reused numbers raise red flags with HMRC. A date-based format such as 2026-0001, 2026-0002 works well because it tells you at a glance when the invoice was raised and keeps your records ordered by year.

Avoid numbering systems that restart at 1 each month unless you include the month reference, for example 2026-03-001. Consistency is what matters most.

Sending invoices to clients

Electronic invoices sent by email as PDF attachments are the accepted and preferred standard for UK clients. Paper invoices are not mandatory. Most clients expect a PDF by email, and this method also gives you a natural digital record of when the invoice was sent.

Tools such as Xero, FreeAgent, and QuickBooks all generate compliant invoices and log send dates automatically. This removes the manual effort and reduces the chance of human error.

How long must you keep records?

| Trader Type | Minimum Retention Period | What to Keep |

|---|---|---|

| Non-VAT sole trader | 5 years after 31 January deadline | Sales invoices, receipts, bank statements |

| VAT-registered sole trader | 6 years | All of the above plus VAT returns and VAT invoices |

These periods run from the 31 january submission deadline of the relevant tax year, not from the date of the invoice itself. A 2023/24 invoice must be kept until at least february 2030 for a non-VAT trader.

Your invoice system should act as the evidence backbone of your business. Store all invoices, bank statements, and supporting documents together and immediately upon issue. This approach, recommended by Tidybill’s record-keeping guidance, simplifies audits and makes your annual tax return far quicker to complete.

Pro Tip: The moment you send an invoice, save a copy to a dedicated folder labelled by tax year. Do not wait until January to organise your records. The five minutes you spend now saves hours later.

How do late payment laws affect sole traders?

The Late Payment of Commercial Debts Regulations 2013 gives sole traders the legal right to charge interest and compensation when a business customer pays late. This is a right most sole traders never use, often because they do not know it exists or because their invoices do not document the terms clearly enough to enforce it.

Here is how the statutory framework works:

- Statutory interest rate. The interest rate is the Bank of England base rate plus 8 percentage points. This applies automatically to business-to-business debts once the agreed payment date passes.

- Fixed compensation fees. You can also claim a fixed fee per unpaid invoice. The fee is £40 for debts under £1,000, £70 for debts between £1,000 and £9,999, and £100 for debts of £10,000 or more.

- Default payment terms. If your invoice does not specify a payment date, the law sets a default of 30 days for public sector customers and 30 days for business customers unless a different term is agreed.

Late payment remedies rely heavily on having full, accurate invoice documentation upfront. Clear documentation maximises your enforcement power and removes ambiguity in disputes. — UK Government late payment framework

To make these rights usable, your invoices must clearly state the payment due date, the consequences of late payment, and your bank details. Vague invoices weaken your position considerably. A sole trader who invoices a design agency for £2,500 and receives payment 45 days late on a 14-day term can legitimately claim statutory interest plus the £70 compensation fee. That is real money, and it is yours by law.

Understanding sole trader taxation rules in the context of late payment also matters. Interest income from late payment claims is taxable, so keep a record of any amounts claimed.

What common invoicing mistakes should sole traders avoid?

Most invoicing problems are avoidable. They tend to fall into a small number of recurring patterns that Cwabc sees regularly when working with new clients.

- Missing your legal name. Trading under a business name without showing your legal name is a compliance failure. HMRC needs to identify the legal entity behind every transaction.

- Charging VAT before registration. This is one of the most serious errors a sole trader can make. If you are not VAT-registered, your invoice must show no VAT whatsoever. Charging it without a registration number is fraudulent.

- Gaps or reused invoice numbers. A missing number in your sequence suggests a transaction has been hidden. Even if accidental, it creates suspicion during an audit.

- Vague or absent payment terms. “Payment on receipt” is not a legally defined term. State a specific number of days, for example “payment due within 14 days of invoice date.”

- Confusing the invoice date with the supply date. These are separate fields. Mixing them up causes VAT reporting errors for registered traders and creates confusion in disputes.

- Deleting or losing old invoices. Keeping records only until the work feels finished is a common mistake. The legal minimum is five years after the relevant 31 january deadline.

- Not including late payment terms. If your invoice does not reference your right to charge statutory interest, you are not prevented from claiming it, but the process becomes harder to enforce.

Pro Tip: Run a quick five-point check before sending every invoice: legal name present, invoice number sequential, supply date separate from invoice date, payment terms stated, and VAT fields correct for your registration status. This takes 30 seconds and prevents the most common errors.

For sole traders managing their own cash basis accounting, accurate invoicing is especially important because income is recorded when payment is received rather than when the invoice is raised. Your invoice date and payment date both need to be clearly documented.

Key takeaways

Sole trader invoicing compliance requires the right information on every invoice, correct VAT treatment based on registration status, and disciplined record-keeping for at least five years.

| Point | Details |

|---|---|

| Mandatory invoice fields | Every invoice must include legal name, sequential number, supply date, description, amounts, and payment terms. |

| VAT invoice differences | VAT-registered traders must add their VAT number, tax point, rate per item, and total VAT to every invoice. |

| Record retention periods | Non-VAT traders keep records for 5 years; VAT-registered traders keep records for 6 years after the relevant deadline. |

| Late payment rights | You can charge Bank of England base rate plus 8 percentage points in interest and fixed fees of £40 to £100 per unpaid invoice. |

| Common mistakes to avoid | Missing legal names, charging VAT before registration, and gaps in invoice numbering are the most frequent compliance failures. |

Why invoicing discipline is worth more than you think

I have worked with sole traders at every stage, from someone invoicing their first client to established freelancers turning over six figures. The pattern I see most often is this: people treat invoicing as an afterthought. They focus on doing the work, and the paperwork gets done quickly, inconsistently, or not at all.

The problem is that HMRC’s invoicing rules exist for a specific reason. HMRC’s focus is on auditability, meaning every invoice needs to answer three questions clearly: what was supplied, when was it supplied, and between whom. If your invoices cannot answer those three questions, you are exposed.

What I have found is that the sole traders who struggle most at tax time are not the ones with complicated finances. They are the ones with inconsistent invoicing habits. A missing supply date here, a reused invoice number there, and suddenly your Self Assessment becomes a detective exercise rather than a straightforward submission.

The good news is that fixing this takes very little time. A solid invoice template, a consistent numbering system, and a digital folder organised by tax year will cover 90% of what HMRC expects. Tools like Xero and FreeAgent make this even easier by automating the numbering and storing sent invoices automatically.

My honest advice is to set your system up once, properly, and then trust it. Do not reinvent your invoicing process every year. Consistency is what protects you, and it is what makes the whole experience of running your finances far less stressful.

— Chris

How Cwabc can take the stress out of your invoicing

Invoicing compliance is straightforward when you have the right system in place. Cwabc works with sole traders across Tonbridge and Kent to set up practical, compliant invoicing processes from day one, covering everything from invoice templates and VAT registration to Making Tax Digital readiness.

Whether you are just starting out or trying to untangle years of inconsistent records, Cwabc offers clear, jargon-free support tailored to your situation. Explore the bookkeeping services in Tonbridge to see how hands-on support can keep your invoicing accurate and your records audit-ready. You can also browse the bookkeeping FAQs for small businesses for quick answers to the questions sole traders ask most often.

FAQ

What information must a sole trader include on an invoice?

Every sole trader invoice must include your legal name and trading name, your address, the customer’s details, a unique sequential invoice number, the invoice date, the supply date, a description of goods or services, itemised amounts, the total owed, and clear payment terms.

Do sole traders have to charge VAT on invoices?

Non-VAT-registered sole traders must not charge or show VAT on invoices. Only traders who are registered for VAT with HMRC may include VAT charges, and they must display their VAT registration number on every VAT invoice.

How long must a sole trader keep invoices?

Non-VAT-registered sole traders must keep records for at least five years after the 31 january deadline of the relevant tax year. VAT-registered sole traders must retain records for six years.

What is the tax point on a VAT invoice?

The tax point, also called the time of supply, is the date on which the goods or services were actually provided. This date can differ from the invoice date and must be recorded separately for accurate VAT reporting.

Can a sole trader charge interest on late payments?

Yes. Under the Late Payment of Commercial Debts Regulations 2013, sole traders can charge statutory interest at the Bank of England base rate plus 8 percentage points, plus a fixed compensation fee of £40, £70, or £100 depending on the size of the debt.